http://www.iaeme.com/IJM/index.asp 43 editor@iaeme.com

International Journal of Management (IJM)

Volume 7, Issue 6, September–October 2016, pp.43–50, Article ID: IJM_07_06_006

Available online at

http://www.iaeme.com/ijm/issues.asp?JType=IJM&VType=7&IType=6

Journal Impact Factor (2016): 8.1920 (Calculated by GISI) www.jifactor.com

ISSN Print: 0976-6502 and ISSN Online: 0976-6510

© IAEME Publication

A STUDY OF FINANCIAL LITERACY AND ITS

IMPACT ON CUSTOMER SATISFACTION WITH

SPECIAL REFERENCE TO BANKS OF BAGALKOT

DISTRICT

Prof. P. K. Gupta

Research scholar, Kousali Institute of Management Studies,

Karnatak University Dharwad, India.

Dr. U. M. Kinange

Professor, Kousali Institute of Management Studies,

Karnatak University Dharwad, India.

ABSTRACT

Financial literacy in simple words is the knowledge about various financial products. Financial

literacy is considered to be an important tool to achieve financial inclusion and hence inclusive

growth. It enables an individual to understand his financial need and hence plan accordingly. The

knowledge of financial concepts is essential for personal financial planning. The S&P Global Fin

Lit Survey shows that Country-level financial literacy ranges from 13% to 71%. Hence the main

objective of this study is to measure the financial literacy of the respondents.

In this study a set of research questions were asked to the respondents to identify the impact of

financial literacy on customer satisfaction towards banking services. It was found that level of

financial literacy was low among the respondents and there is no significant impact of financial

literacy on overall customer satisfaction.

Key words: Financial literacy, financial inclusion, and customer satisfaction.

Cite this Article: P. K. Gupta and Dr. U. M. Kinange, A Study of Financial Literacy and its Impact

on Customer Satisfaction with Special Reference to Banks of Bagalkot District. International

Journal of Management, 7(6), 2016, pp. 43–50.

http://www.iaeme.com/IJM/issues.asp?JType=IJM&VType=7&IType=6

1. INTRODUCTION

The Organization for Economic Co-operation and Development (OECD) has defined financial literacy as

“a combination of awareness, knowledge, skill, attitude and behavior necessary to make sound financial

decisions and ultimately achieve individual wellbeing”.

Financial literacy in simple words is the knowledge about various financial products. Financial literacy

is considered to be an important tool to achieve financial inclusion and hence inclusive growth. It enables

P. K. Gupta and Dr. U. M. Kinange

http://www.iaeme.com/IJM/index.asp 44 editor@iaeme.com

an individual to understand his financial need and hence plan accordingly. Therefore the knowledge of

financial concepts is essential for personal financial planning.

The research conducted by various organisations indicated low level of financial literacy across the

globe. The S&P Global Fin Lit Survey found that worldwide only 33.33% of the adults are financial

literate. Further only 27% of the adults are financial literate in Asia. The policy makers across the globe

have expressed concerns about the low level of financial literacy. Hence in 2008, the Organisation for

Economic Co-operation and Development (OECD) has created an International Network on Financial

Education (INFE) to tackle the issue of financial literacy by creating an international platform for policy

makers.

Customer satisfaction is a frequently used term in marketing. It is a measure of how products and

services of a company meet customer expectation. “Customer satisfaction is the key for many banks to

survive in competition” (Mistry, D. S. H., 2013).

2. REVIEW OF LITERATURE

2.1. Financial Literacy

Volpe et al. (2002) measured investment literacy of 530 online investors and found that level of investment

literacy varied with people’s education, experience, age, income and gender. Men respondents had higher

investment literacy when compared to women respondents.

Cole et al. (2008) measured the level of financial literacy and its relationship to demand for financial

services in India and Indonesia. The study indicated a strong relationship between financial literacy and the

demand for financial products.

Al-Tamimi and Kalli (2009) assessed the financial literacy of the UAE investors. The results indicate

that the financial literacy of respondents is far below the needed level. The study also found that financial

literacy is affected by income level, education level and workplace-activity.

Almenberg and Soderbergh (2011) investigated the relationship between financial literacy and

retirement planning of Swedish adults. It was found that there exist a significant difference in financial

literacy between planners and non-planners. Financial literacy level was found lower among older people,

women and those with low education or earnings.

2.2. Customer Satisfaction

Padhy, P. K., & Swar, B. N. (2009) made an empirical study of major quality improvement initiatives

recently undertaken by two banks. The primary aim of the study was to enhance the understanding of

service quality and to identify models that can be employed by the managers in service industry. The

researcher investigated the role that technology played in banking and its impact on the delivery of

perceived service quality. The SERVQUAL measuring instrument was used for the research. Three groups

of banks (Private-ICICI and Axis Bank; Public - SBI and PNB; & Foreign Bank – Citi bank) were selected

for the study, which was conducted in Orissa. Primary data was collected from a sample of 440

respondents on judgmental basis of which 300 useable questionnaires were analyzed. It was found that

service quality in public sector banks in India is poor. On the selected five dimensions foreign banks

followed by private sector banks performed better than public sector banks.

Dawar (2013) made an attempt to identify the main factors that influence the customer satisfaction in

retail banking. A comparative research design has been chosen to elucidate the determinants of Customer

Satisfaction. Factor Analysis was used for data analysis. The researcher applied KMO (Kaiser-Meyer-

Olkin) and Bartlett's Test to the collected data. Kaiser-Meyer-Olkin Measure of Sampling Adequacy test

shows the value of .814. The researcher concluded his study by identifying factors that may be used by the

bankers of small town to identify drive customer loyalty out of customer satisfaction.

A Study of Financial Literacy and its Impact on Customer Satisfaction with Special Reference to Banks of

Bagalkot District

http://www.iaeme.com/IJM/index.asp 45 editor@iaeme.com

Nippatlapalli, A. R. (2013) conducted a study to identify the factors that influences the customer

behavior of SBI and to study the Satisfaction of customers towards the bank. The study was undertaken at

Kavali region of Andhra Pradesh state with a sample size of 200. It was found that the customers were less

aware about online transactions facilities provided by the bank. Further it was observed that the 84% of the

Respondents were satisfied on financial transactions of the Bank.

3. OBJECTIVES OF THE STUDY

• To measure the level of financial literacy among the respondents.

• To measure the customer satisfaction of respondents.

• To study the impact of financial literacy on customer satisfaction towards banking services.

4. RESEARCH METHODOLOGY

The title of the study is “A Study of Financial Literacy and its Impact on Customer Satisfaction with

Special Reference to Banks of Bagalkot District”. The Research Methodology is a blend of primary and

secondary data.

The questionnaire drafted by FINRA Investor Education Foundation consisting of five-questions is

considered to test financial literacy and the questionnaire of Sabir, R. I., et al. 2014 has been considered for

determining the customer satisfaction, with some modifications to accomplish the objective of this study.

The data was analysed using means and combined means.

4.1. Data Collection

• Secondary Data: The secondary data includes an analysis of research works carried out on financial literacy

in the past.

• Primary Data: The primary data is collected using a questionnaire to translate the defined research objective.

4.2. Sampling Framework

• Population –Bagalkot district of Karnataka

• Sampling Unit – Members of Self Help Groups

• Sampling Method – Random sampling.

• Sample size: 60.

5. ANALYSIS AND INTERPRETATION

The required data has been collected by way of a questionnaire and it has been analyzed and interpreted

with the help of tables with relevant descriptions.

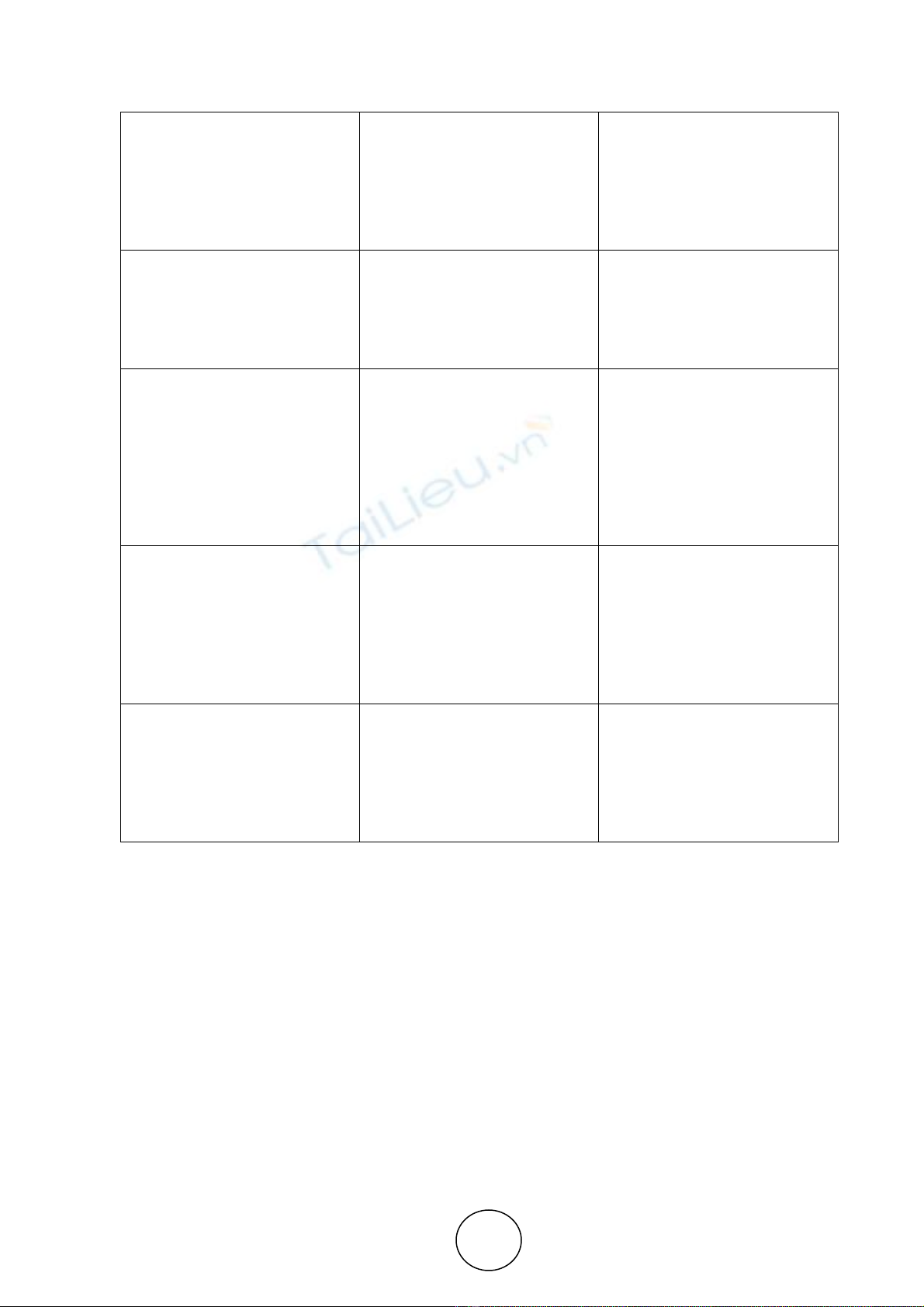

Table 1 Demographic Variables

Demographic Variables No. of Respondents Percentage

Gender

Male

Female

11

49

18.33

81.67

Age

Under 20

21 – 30 years

31 – 40 years

41 – 50 years

50-60 years

60 and Above

0

3

15

21

16

5

0

5

25

35

26.67

8.33

P. K. Gupta and Dr. U. M. Kinange

http://www.iaeme.com/IJM/index.asp 46 editor@iaeme.com

Educational Level

Primary

Secondary

Higher Secondary

Undergraduate

Graduate

Post Graduate

32

9

7

0

12

0

53.33

15

11.67

0

20

0

Profession:

Business

Service

Student

House wife

Others

13

17

4

17

9

21.67

28.33

6.67

28.33

15

Monthly Income (Rs.)

Below 10,000

10,000 - 20,000

20,000 - 50,000

50,000 – 75,000

75,000 – 100,000

100,000 – 200,000

200,000 – 400,000

400,000 and above

30

12

4

2

2

0

7

3

50

20

6.67

3.33

3.33

0

11.67

5

Duration of Bank Accounts

Operated by the Respondents

Less than 1 Year

1-3 Years

3-5 Years

5-10 Years

More than 10 years

1

11

15

30

3

1.67

18.33

25

50

5

Frequency of Using Banking

Services

Daily

Once in a week

Once in 2 weeks

Once in 3 weeks

Once in a Month

0

1

1

9

49

0

1.67

1.67

15

81.67

The table 1 reveals that 49 (81.67%) respondents surveyed were females and 11(18.33) were male.

Most of the respondents 21 (35%) belong to the age group of 41 to 50 years. The literacy level speaks the

full facts a) Primary level - 32 (53.33%), b) Secondary level - 9 (15%), c) higher secondary level - 7

(11.67%), d) under graduate level – 0 (0 %), and e) graduate level – 12 (20%). Among the occupational

categories, 17 (28.33%) respondents were house wife, 17 (28.33%) were in service, 13 (21.67%) are

businessmen, 4 (6.67%) were student and 9 (15%) belonged to other categories.

The income wise classification showed that the 30 (50%) were in below Rs 10,000 group. 12 (20%)

were in the 10,000 to 20, 000 group, 4 (6.67%) were in the 20,000 to 50,000 group, 2 (3.33%) were in the

50,000 to 75,000 group, 2 (3.33%) were in the 75,000 to 100,000 group, 7(11.67%) in 2,00,000 to 4,00,000

group and 3 (5%) belongs to the group of 4,00,000 and above.

Only 1 (1.67%) respondent was dealing with bank for less than one year, 11 (18.33%) were having

account between 1-3 year, while 15 (25%) were dealing with this bank for 3 to 5 years. 30 (50%) were

account holders for 5 to 10 years and 3 (5%) were dealing with the bank for more than 10 years. Out of the

60 respondents selected for study, no respondent used banking services daily, 1 (1.67%) respondent used

A Study of Financial Literacy and its Impact on Customer Satisfaction with Special Reference to Banks of

Bagalkot District

http://www.iaeme.com/IJM/index.asp 47 editor@iaeme.com

banking once in a week, 1(1.67%) respondent used banking once in two weeks, 9 (15%) were banking

once in three weeks, and 49 (81.67%) were banking once in a month.

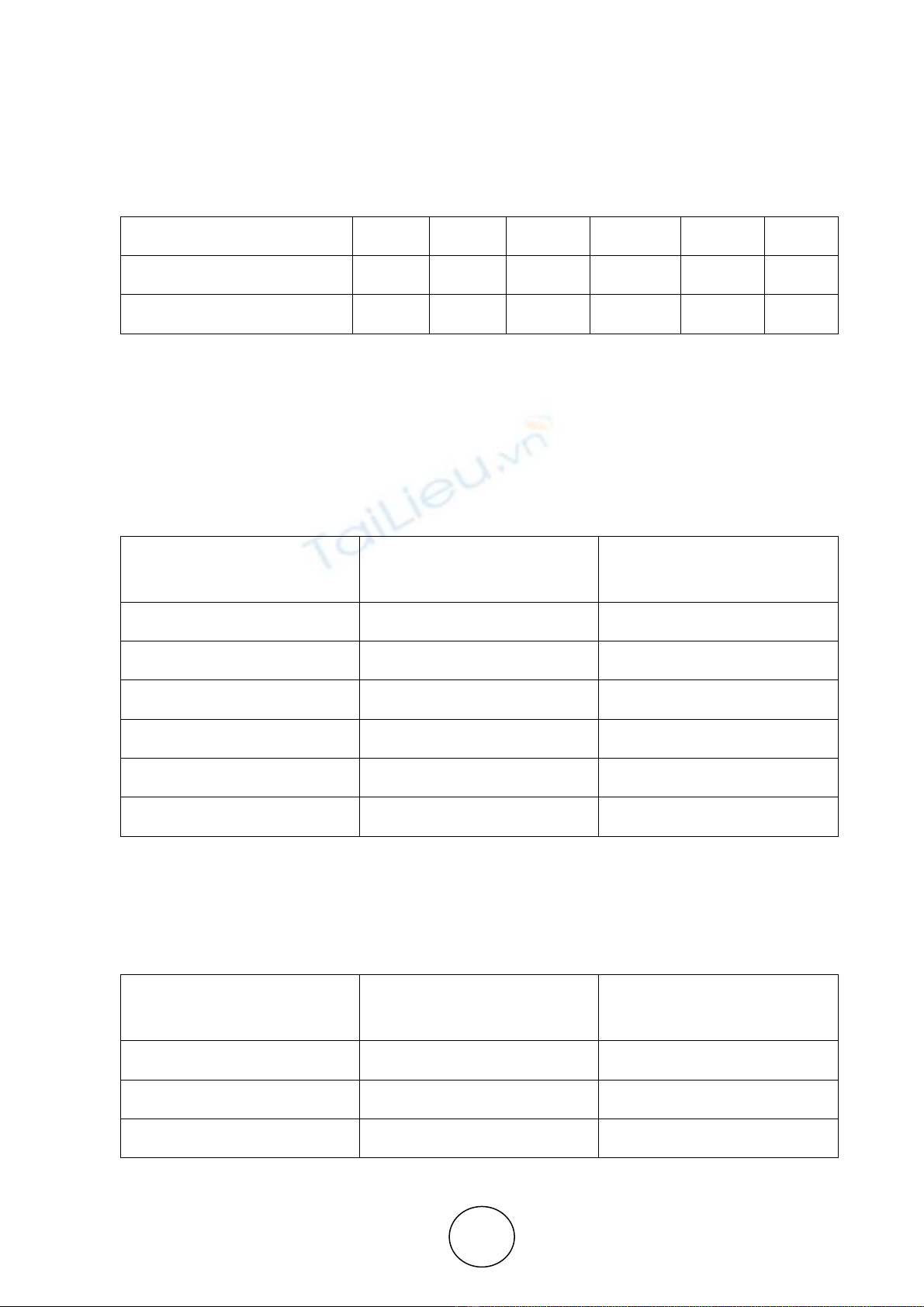

Table 2 Percentage of respondents giving correct answer on financial literacy questions.

No. of Correct Answer 0 1 2 3 4 5

Number of Respondents 10 14 14 12 5 5

Percentage of Respondents 16.67 23.33 23.33 20 8.33 8.33

Table No. 2 shows that 5 (8.33%) respondents have answered all the questions correctly. Further 5

(8.33%) respondents have answered four of the questions correctly, 12 (20%) respondents have answered

three questions correctly, 14 (23.33%) have answered only 2 questions correctly. 14 (23.33%) of the

respondents have answered only one question correctly. 10 (16.67%) of the respondents answered all the

questions in a wrong way. Hence only 22 (36.67%) respondents have given correct answer for minimum

three questions and are considered to be having higher level of financial literacy when compared to

remaining 38 (63.33%) respondents.

Table 3 Perceptions of Customers about banks Tangibility

Dimensions Respondents with high

Financial Literacy Level

Mean

Respondents with low

Financial Literacy Level

Mean

Premises 4.27 4.45

Technology 4.50 4.37

Employee Dress 4.14 4.13

Complete Information 3.82 3.82

Bank Statement 3.82 3.85

Combined Mean 4.11 4.06

The data in Table-3 brings to light the difference in the perceptions of the customers on tangibles. The

data reveals that the combined mean of respondents with high financial literacy level is 4.11 and with low

financial literacy level is 4.06. It clearly shows that level of financial literacy has very low impact on the

tangibility factor of customer satisfaction.

Table 4 Perceptions of Customers about banks reliability factor

Dimensions Respondents with high

Financial Literacy Level

Mean

Respondents with low

Financial Literacy Level

Mean

Service of bank 4.00 3.92

Handling a problem 3.73 3.58

Satisfied with bank service 3.50 3.63

![Vay vốn Agribank: Điều kiện và thủ tục [mới nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2020/20200720/mami89/135x160/7951595232152.jpg)

![Ngân hàng câu hỏi trắc nghiệm Lý thuyết Tài chính - Tiền tệ: Học phần [Mô tả thêm về nội dung học phần nếu có]](https://cdn.tailieu.vn/images/document/thumbnail/2025/20251003/kimphuong1001/135x160/26991759476043.jpg)

![Bài tập Tài chính doanh nghiệp có đáp án [kèm lời giải chi tiết]](https://cdn.tailieu.vn/images/document/thumbnail/2025/20250927/aimy1105nd@gmail.com/135x160/92021759119232.jpg)