Utilitarian Pricing of Annuities •111

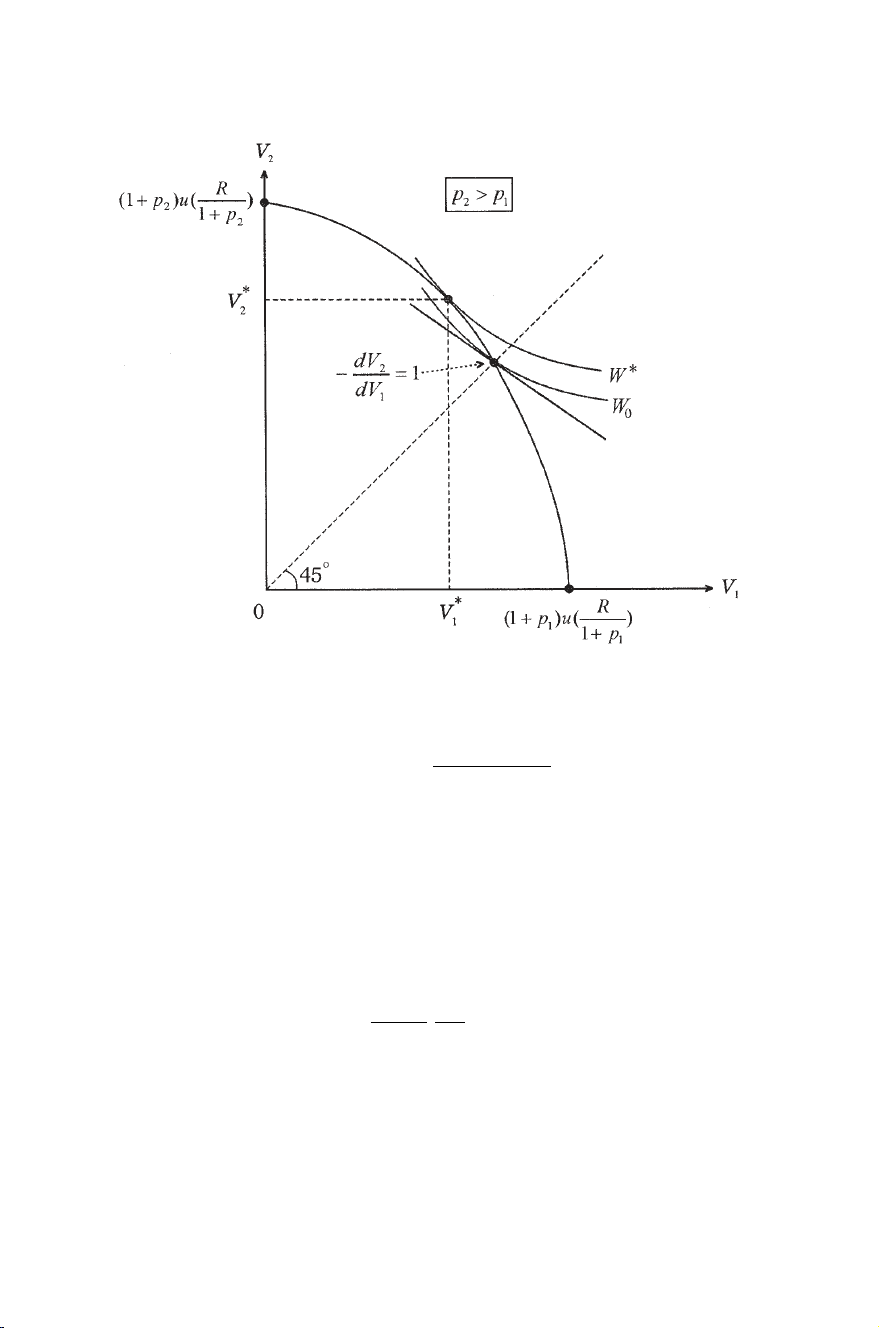

Figure 13.1. First-best allocation of utilities.

while

V∗

h=(1 +ph)uR

H

h=1(1 +ph).

Thus, the utilitarian first best has inequality in expected utilities but may

have equality in consumption levels (Arrow, 1992).

This result is similar to Mirrlees’ (1971) optimum income tax model

where individuals differ in productivity.2The first best allocation pro-

vides higher (expected) utility to those with a higher capacity to produce

utility.

In the appendix to this chapter it is shown that

0>1+pn

c∗

h

∂c∗

h

∂ph

>−1,(13.7)

while ∂c∗

h/∂pj0,for j= h,h,j=1,2,..., n.

2In Mirrlees’ model with additive utilities, the first best has all individuals with equal

consumption, and those with higher productivity, having a lower disutility for generating a

given income, are assigned to work more and hence have a lower utility.

112 •Chapter 13

Concavity of uand (13.7) imply

∂V∗

h

∂ph

=u(c∗

h)+(1 +pn)u′(cn)∂c∗

h

∂pn

>0,(13.8)

while ∂V∗

h/∂pj0,j= h,j=1,2,...,H.3Thus, with the given total

resources, an increase in one individual’s survival probability decreases

his or her optimum consumption, but the positive effect of higher survival

probability on expected utility dominates. The effect on the welfare

of other individuals facing only resource redistribution depends on the

shape of the social welfare function.

13.2Competitive Annuity Market with Full Information

In a competitive market with full information on the survival proba-

bilities of individuals and a zero rate of interest, the price of a unit of

second-period consumption, c2h, is equal to the survival probability of

each annuitant. Individuals maximize expected utility subject to a budget

constraint

c1h+phc2h=yhh=1,2,..., H,(13.9)

where yhis the given income of individual h. Demands for first- and

second-period consumption (annuities),

c1hand

c2h, are given by

c1h=

c2h=

ch=yh/(1 +ph).

The first-best allocation can be supported by a competitive annuity

market accompanied by an optimum income allocation. Equating con-

sumption levels under competition,

ch,to the optimum levels, c∗

h(p),

yields unique income levels,

yh=(1 +ph)c∗

h(p),that support the first-best

allocation. In particular, with an additive W, all individuals consume the

same amount:

c∗

h=R

H

h=1(1 +ph),

hence

yh=1+ph

H

h=1(1 +ph)R.(13.10)

3In the extreme case when W=min[V

1,V

2,...,VH], optimum expected utilities,

V∗

h=(1 +ph)u(c∗

h), are equal, and hence optimum consumption, c∗

h, strictly decreases

with ph(and increases with pj,j= h).

Utilitarian Pricing of Annuities •113

13.3Second-best Optimum Pricing of Annuities

Governments do not engage, for well-known reasons, in unconstrained

lump-sum redistributions of incomes. In contrast, most annuities

are supplied directly by government-run social security systems and

taxes/subsidies can, if so desired, be applied to the prices of annuities

offered by private pension funds. These prices can be used by govern-

ments to improve social welfare. Although deviations from actuarially

fair prices entail distortions (i.e., efficiency losses), distributional im-

provements may outweigh the costs.4

Suppose that individual hpurchases annuities at a price of qh.With

an income yh, his or her budget constraint is

c1h+qhc2h=yh,h=1,2...,H.(13.11)

Maximization of (13.2) subject to (13.11) yields demands

cih =

cih(qh,ph,yh), i=1,2,and h=1,2,...,H. Maximized expected utility,

V

h,is

V

h(qh,ph,yh)=u(

c1h)+phu(

c2h).

Assume that no outside resources are available for the annuity market,

hence total subsidies/taxes must equal zero,

H

h=1

(qh−ph)

c2h=0.(13.12)

Maximization of W(

V

1,

V

2,...,

VH) with respect to prices (q1,...,qH)

subject to (13.12) yields the first-order condition

∂W

∂

V

h

∂

V

h

∂qh

+λ

c2h+(qh−ph)∂

c2h

dqh=0,h=1,2,...,H,(13.13)

where λ>0 is the shadow price of constraint (13.12). In elasticity form,

using Roy’s identity (∂

V

h/∂qh=−(∂

V

h/∂yh)

c2h), (13.13) can be written

qh−ph

qh

=θh

εh

,(13.14)

where εh=−(qh/

c2h)(∂

c2h/dqh)istheprice elasticity of second-period

consumption of individual hand

θh=1−1

λ

∂W

∂

V

h

∂

V

h

∂yh

4In practice, of course, prices do not vary individually. Rather, individuals with similar

survival probabilities are grouped into risk classes, and annuity prices and taxes/subsidies

vary across these classes.

114 •Chapter 13

is the net social value of a marginal transfer to individual hthrough the

optimum pricing scheme. Equation (13.14) is a variant of the well-known

inverse elasticity optimum tax formula, which combines equity (θh) and

efficiency (1/εh) considerations.

The implication of (13.14) for the optimum pricing of annuities

depends on the welfare function, W, and on the joint distribution of

incomes, (y1,...,yH), and probabilities, (p1,..., pH).

To obtain some concrete examples, let Wbe the sum of expected

utilities. Then ∂W/∂

V

h=1,h=1,2,...,H. Assume further that

V

h=ln c1h+phln c2h. In this case, demands are

c1h=yh

1+ph

,

c2h=yh

1+ph

ph

qh

,(13.15)

and

V

h=(1+ph)ln yh

1+ph+phln ph

qh.(13.16)

Conditions (13.14) and (13.12) now yield the solution

qh=φβh

H

h=1βh,(13.17)

where

φ=

H

h=1

ph>0 and βh=phyh

1+ph

>0.

Consider two special cases of (13.17):

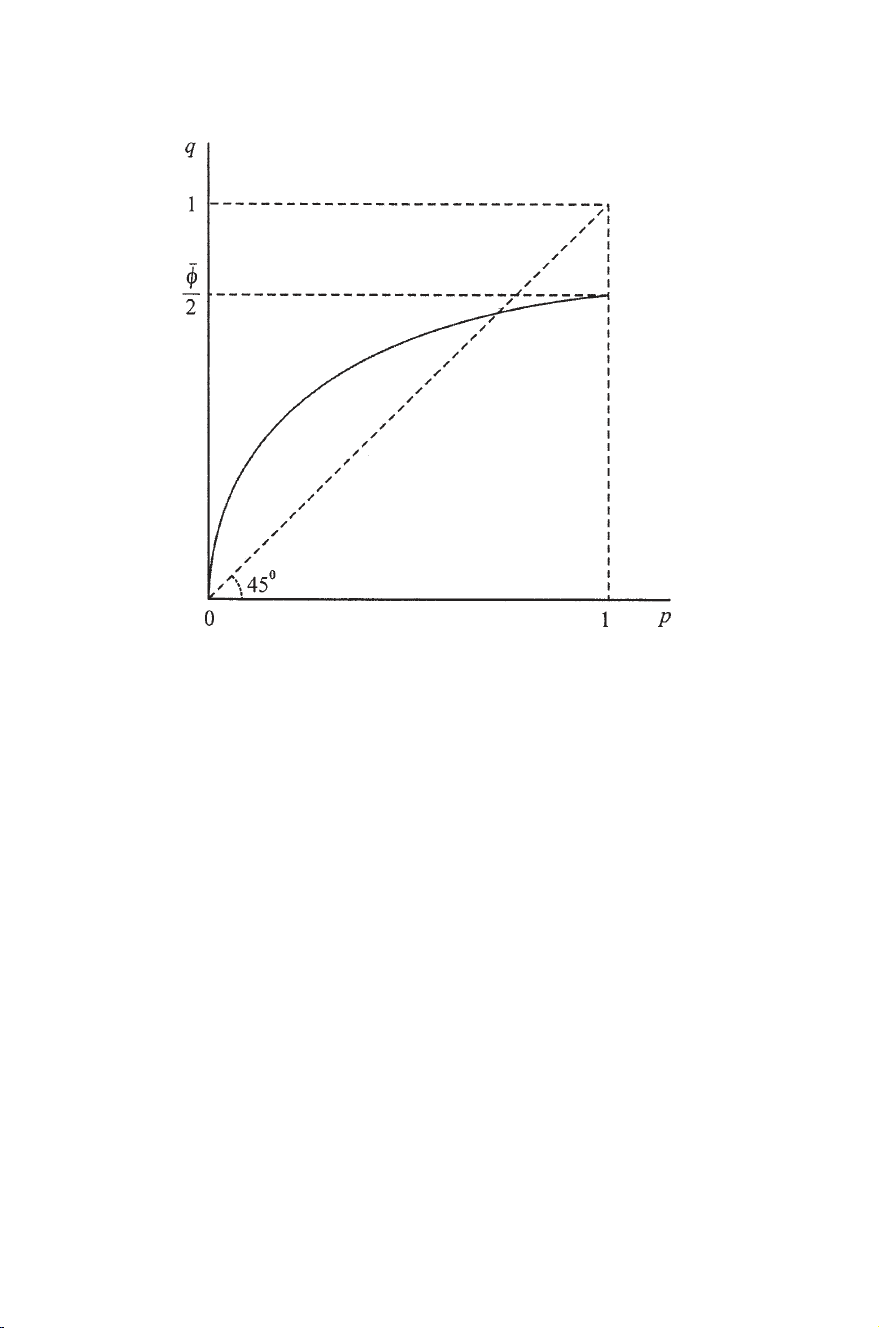

(a) Equal incomes: (yh=y=R/H;h=1,2,...,H)

Condition (13.17) now becomes qh=¯

φ(ph/(1 +ph)),where

¯

φ=H

h=1ph

H

h=1ph

1+ph(>1).(13.18)

It is seen (figure 13.2) that optimum pricing involves subsidization

(taxation) of individuals with high (low) survival probabilities.5

5In figure 13.2, it can be shown that ¯

φ/2<1.

Utilitarian Pricing of Annuities •115

Figure 13.2. Optimum annuity pricing in a full-information equilibrium.

(b) yh=y(1 +ph)

This, one recalls, is the first-best utilitarian income distribution, and since

all price elasticities are equal to unity, we see from (13.17), as expected,

that qh=ph; that is efficiency prices are optimal.

More generally, it is seen from (13.17) that a higher correlation

between incomes, yh, and survival probabilities, ph, decreases—and

possibly eliminates—the subsidization of high-survival individuals.

In contrast, a negative correlation between incomes and survival

probabilities (as, presumably, in the female/male case) leads to subsidies

for high- survival individuals, possibly to the commonly observed

uniform pricing rule.

![Tín dụng trung-dài hạn: Những vấn đề cơ bản [chuẩn nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2013/20131120/butmauden/135x160/6441384999291.jpg)

![Đề thi giữa học kì Tài chính tiền tệ: Tổng hợp [Năm]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260513/hoacattuong2026/135x160/81291778835177.jpg)

![320 câu hỏi trắc nghiệm Nghiệp vụ Ngân hàng có đáp án [Mới nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260407/zinedinezidane06/135x160/49541776134685.jpg)

%20--%3e%3cdefs%3e%3cstyle%3e%20.st0%20{%20fill:%20%23fff;%20}%20.st1%20{%20fill:%20%237800fa;%20}%20%3c/style%3e%3c/defs%3e%3cpath%20class='st1'%20d='M117.78,12.18H43.11c2.9,3.47,4.65,7.94,4.65,12.82,0,5.6-2.3,10.66-6.01,14.29h76.02l7.22-13.56-7.22-13.56Z'/%3e%3cg%3e%3cpath%20class='st0'%20d='M53.58,26.17h-.59v-1.46h.59v-4.96h2.83c1.78,0,2.67.94,2.67,2.82v5.76c0,1.87-.89,2.81-2.67,2.81h-2.83v-4.96ZM55.36,21.37v3.34h1.1v1.46h-1.1v3.34h1.01c.61,0,.91-.37.91-1.1v-5.93c0-.74-.3-1.1-.91-1.1h-1.01Z'/%3e%3cpath%20class='st0'%20d='M65.99,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM65.28,18.04c-.25.46-.51.77-.75.94-.21.15-.47.22-.79.22-.26,0-.57-.07-.92-.22l-.38-.15c-.14-.05-.26-.07-.37-.07-.3,0-.53.18-.71.54l-.91-.68c.25-.46.51-.77.75-.94.21-.14.48-.21.79-.21.26,0,.57.07.92.21l.38.15c.14.05.26.07.37.07.3,0,.53-.18.71-.54l.91.68ZM61.91,27.52h1.73l-.87-5.76-.87,5.76Z'/%3e%3cpath%20class='st0'%20d='M74.53,26.89v1.52c0,1.91-.89,2.86-2.67,2.86s-2.67-.95-2.67-2.86v-5.93c0-1.91.89-2.86,2.67-2.86s2.67.95,2.67,2.86v1.11h-1.69v-1.22c0-.75-.31-1.12-.93-1.12s-.93.37-.93,1.12v6.15c0,.74.31,1.11.93,1.11s.93-.37.93-1.11v-1.63h1.69Z'/%3e%3cpath%20class='st0'%20d='M81.4,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM75.9,19.2l1.52-1.91h1.71l1.51,1.91h-1.61l-.76-.95-.75.95h-1.61ZM77.32,27.52h1.73l-.87-5.76-.87,5.76ZM83.1,15.99l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M84.86,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM84.01,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M93.51,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM92.66,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M98.8,31.14h-1.79v-11.39h1.79v4.88h2.03v-4.88h1.83v11.39h-1.83v-4.88h-2.03v4.88Z'/%3e%3cpath%20class='st0'%20d='M105.36,24.55h2.46v1.62h-2.46v3.34h3.09v1.63h-4.88v-11.39h4.88v1.63h-3.09v3.18ZM108.17,17.29l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M112.2,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM111.35,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3c/g%3e%3ccircle%20class='st1'%20cx='25'%20cy='25'%20r='20'/%3e%3cpath%20class='st0'%20d='M32.78,19.27c2.92,0,4.43,2.55,5.28,5.33l.71,2.17c.14.38-.33.75-.71.75h-5.61c.19-.33.24-.71.09-1.08l-.75-2.45c-.43-1.32-.99-2.64-1.79-3.77.75-.57,1.65-.94,2.78-.94h0ZM25,18.38c3.25,0,4.9,2.78,5.89,5.89l.76,2.45c.14.42-.33.8-.8.8h-11.69c-.42,0-.94-.38-.8-.8l.75-2.45c.99-3.11,2.64-5.89,5.89-5.89h0ZM25,11.35c1.74,0,3.11,1.37,3.11,3.11s-1.37,3.11-3.11,3.11-3.11-1.41-3.11-3.11,1.41-3.11,3.11-3.11h0ZM17.27,19.27c1.08,0,1.98.38,2.73.94-.8,1.13-1.37,2.45-1.74,3.77l-.8,2.45c-.14.38-.05.75.09,1.08h-5.56c-.42,0-.9-.38-.75-.75l.71-2.17c.9-2.78,2.41-5.33,5.33-5.33h0ZM17.27,12.91c1.51,0,2.78,1.27,2.78,2.83s-1.27,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM32.78,12.91c1.56,0,2.78,1.27,2.78,2.83s-1.23,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM27.07,28.56v.09c0,.57-.24,1.08-.61,1.46h0v.05c-.38.33-.9.57-1.46.57s-1.08-.24-1.46-.61h0c-.38-.38-.61-.9-.61-1.46v-.09h1.41v.09c0,.19.05.38.19.47v.05c.09.09.28.19.47.19s.38-.09.47-.19v-.05c.14-.09.24-.28.24-.47t-.05-.09h1.41ZM30.99,28.56v.09c0,1.65-.66,3.16-1.74,4.24-1.08,1.08-2.59,1.79-4.24,1.79s-3.16-.71-4.24-1.79l-.05-.05c-1.04-1.08-1.7-2.55-1.7-4.2v-.09h1.41v.09c0,1.27.47,2.4,1.27,3.25h.05c.85.85,1.98,1.37,3.25,1.37s2.4-.52,3.25-1.37c.85-.8,1.37-1.98,1.37-3.25v-.09h1.37ZM34.99,28.56v.09c0,2.78-1.13,5.28-2.92,7.07-1.79,1.79-4.29,2.92-7.07,2.92s-5.23-1.13-7.07-2.92c-1.79-1.79-2.92-4.29-2.92-7.07v-.09h1.41v.09c0,2.4.94,4.53,2.5,6.08,1.56,1.56,3.72,2.5,6.08,2.5s4.52-.94,6.08-2.5c1.56-1.56,2.5-3.68,2.5-6.08v-.09h1.41Z'/%3e%3c/svg%3e)