CHAPTER 28

Managing International Risks

Answers to Practice Questions

1. Answers here will vary, depending on when the problem is assigned.

2. a. The dollar is selling at a forward premium on the baht.

b.

c. Using the expectations theory of exchange rates, the forecast is:

$1 = 44.555 baht

d. 100,000 baht = $(100,000/44.555) = $2,244.42

3. We can utilize the interest rate parity theory:

If the three-month rand interest rate were substantially higher than 5.07%, then

you could make an immediate arbitrage profit by buying rands, investing in a

three-month rand deposit, and selling the proceeds forward.

4. Answers will vary depending on when the problem is assigned. However, we can

say that if a bank has quoted a rate substantially different from the market rate,

an arbitrage opportunity exists.

5. Our four basic relationships imply that the difference in interest rates equals the

expected change in the spot rate:

We would expect these to be related because each has a clear relationship with

the difference between forward and spot rates.

45

1.89%.018901

44.345

44.555

4==

−×

5.07%0.0507r

8.3693

8.4963

1.035

r1

rand

rand ==⇒=

+

L/$

L/$

L/$

L/$

$

L

s

)(sE

s

f

r1

r1 ==

+

+

$/rand

$/rand

$

rand

s

f

r1

r1 =

+

+

6. If international capital markets are competitive, the real cost of funds in Japan must

be the same as the real cost of funds elsewhere. That is, the low Japanese yen

interest rate is likely to reflect the relatively low expected rate of inflation in Japan

and the expected appreciation of the Japanese yen. Note that the parity

relationships imply that the difference in interest rates is equal to the expected

change in the spot exchange rate. If the funds are to be used outside Japan, then

Ms. Stone should consider whether to hedge against changes in the exchange rate,

and how much this hedging will cost.

7. a. Exchange exposure. Compare the effect of local financing with the export

of capital from the U.S.

b. Capital market imperfections. Some countries use exchange controls to

force the domestic real interest rate down; others offer subsidized loans to

foreign investors.

c. Taxation. If the subsidiary is in a country with high taxes, the parent may

prefer to provide funds in the form of a loan rather than equity.

d. Government attitudes to remittance. Interest payments, royalties, etc.,

may be less subject to control than dividend payments

e. Expropriation risk. Although the host government might be ready to

expropriate a venture that was wholly financed by the parent company, the

government may be reluctant to expropriate a project financed directly by

a group of leading international banks.

f. Availability of funds, issue costs, etc. It is not possible to raise large sums

outside the principal financial centers. In other cases, the choice may be

affected by issue costs and regulatory requirements. For example,

Eurodollar issues avoid SEC registration requirements.

8. Suppose, for example, that the real value of the deutschemark (DM) declines

relative to the dollar. Competition may not allow Lufthansa to raise trans-Atlantic

fares in dollar terms. Thus, if dollar revenues are fixed, Lufthansa will earn fewer

DM. This will be offset by the fact that Lufthansa’s costs may be partly set in dollars,

such as the cost of fuel and new aircraft. However, wages are fixed in DM. So the

net effect will be a fall in DM profits from its trans-Atlantic business.

However, this is not the whole story. For example, revenues may not be wholly

in dollars. Also, if trans-Atlantic fares are unchanged in dollars, there may be

extra traffic from German passengers who now find that the DM cost of travel has

fallen.

In addition, Lufthansa may be exposed to changes in the nominal exchange rate.

For example, it may have bills for fuel that are awaiting payment. In this case, it

would lose from a rise in the dollar.

46

Note that Lufthansa is partly exposed to a commodity price risk (the price of fuel

may rise in dollars) and partly to an exchange rate risk (the rise in fuel prices may

not be offset by a fall in the value of the dollar). In some cases, the company

can, to a great extent, fix the dollar cash flows, such as by buying oil futures.

However, it still needs at least a rough-and-ready estimate of the hedge ratios,

i.e., the percentage change in company value for each 1% change in the

exchange rate. (Hedge ratios are discussed in Chapter 27.) Lufthansa can then

hedge in either the exchange markets (forwards, futures, or options) or the loan

markets.

9. Suppose a firm has a known foreign currency income (e.g., a foreign currency

receivable). Even if the law of one price holds, the firm is at risk if the overseas

inflation rate is unexpectedly high and the value of the currency declines

correspondingly. The firm can hedge this risk by selling the foreign currency

forward or borrowing foreign currency and selling it spot. Note, however, that this

is a relative inflation risk, rather than a currency risk; e.g., if you were less certain

about your domestic inflation rate, you might prefer to keep the funds in the

foreign currency.

If the firm owns a foreign real asset (like Outland Steel’s inventory), your worry is

that changes in the exchange rate may not affect relative price changes. In other

words, you are exposed to changes in the real exchange rate. You cannot so

easily hedge against these changes unless, say, you can sell commodity futures

to fix income in the foreign currency and then sell the currency forward.

10.The dealer estimates the following relationship in order to calculate the hedge ratio

(delta):

Expected change in company value = a + (δ × Change in value of yen)

For the Ford dealer:

Expected change in company value = a + (5 × Change in value of yen)

Thus, to fully hedge exchange rate risk, the dealer should sell yen forward in an

amount equal to one-fifth of the current company value.

47

11.The future cash flows from the two strategies are as follows:

Sell Euro Forward

Euro Appreciates to

$0.92/euro

Euro Depreciates to

$0.89/euro

i. Do not receive order

(must buy euros at future

spot rate to settle

contract)

1,000,000 (0.9070)

- 1,000,000 (0.92)

= -$13,000

1,000,000 (0.9070)

- 1,000,000 (0.89)

= $17,000

ii. Receive order (deliver)

(inflow of 1,000,000 euros

to settle contract)

1,000,000 (0.9070)

= $907,000

1,000,000 (0.9070)

= $907,000

Buy 6-Month

Put Option

Euro Appreciates to

$0.92/euro

Euro Depreciates to

$0.89/euro

i. Do not receive order

(if euro depreciates, buy

euros at future spot rate

and exercise put)

$0 1,000,000 (0.9070)

- 1,000,000 (0.89)

= $17,000

ii. Receive order

(sell euros received at the

higher of the spot or put

exercise price)

1,000,000 (0.92)

= $920,000

1,000,000 (0.9070)

= $907,000

Note that, if the firm is uncertain about receiving the order, it cannot completely

remove the uncertainty about the exchange rate. However, the put option does

place a downside limit on the cash flow although the company must pay the

option premium to obtain this protection.

12. a. Pesos invested = 1,000 × 500 pesos = 500,000 pesos

Dollars invested = 500,000/9.1390 = 54,710.58

b.

Dollars received = (550 × 1000)/9.5 = 57,894.74

c. There has been a return on the investment of 10% but a loss on the

exchange rate.

48

10.0%0.10

1000500

(1000)500)(550

pesosinreturnTotal ==

×

×−

=

5.82%0.0582

54,710.58

54,710.5857,894.74

dollarsinreturnTotal ==

−

=

13.The nominal exchange rate is given in the table in the statement of the problem.

The real exchange rate is equal to the nominal exchange rate multiplied by the

inflation differential. (See footnote 15, p. 795 of the text.)

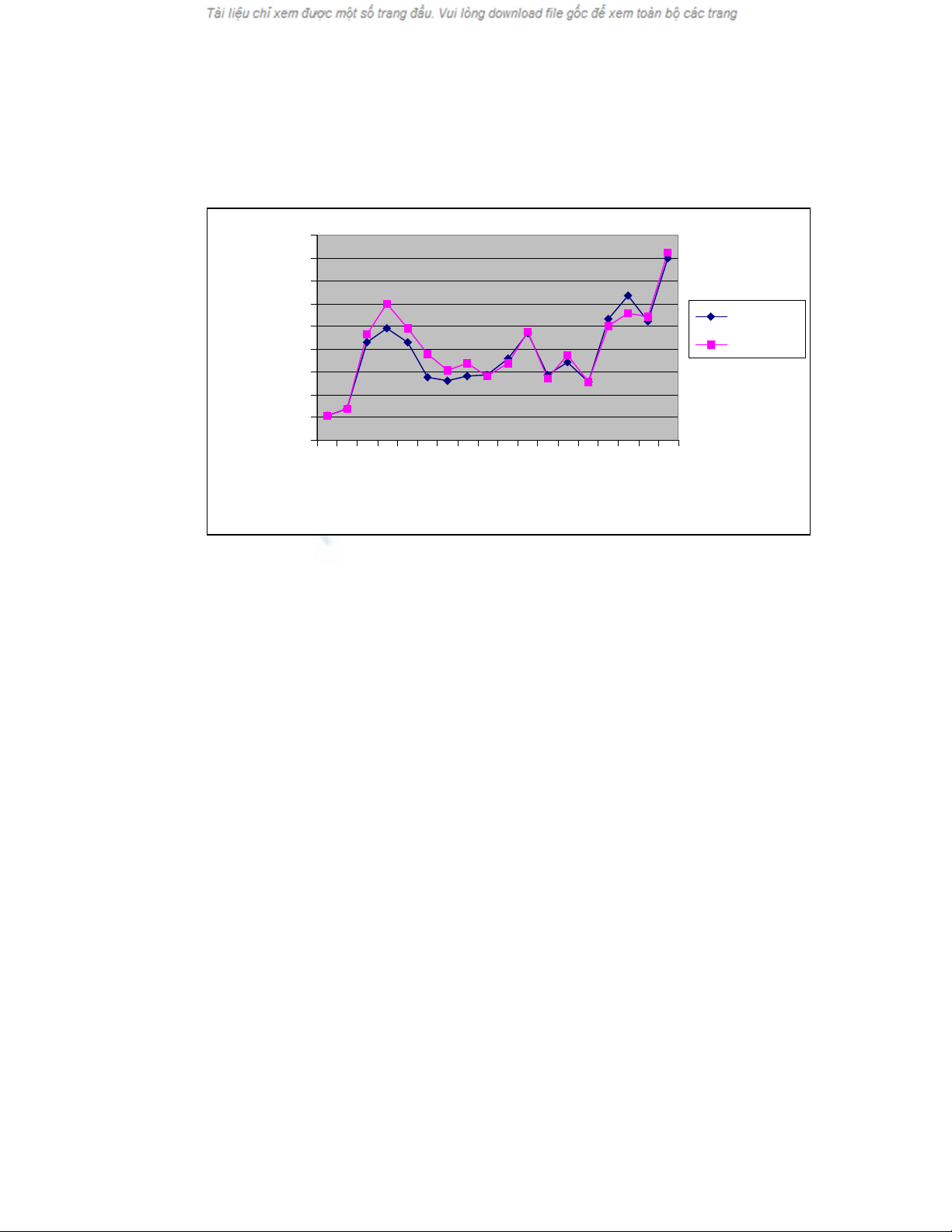

14. George lives in the U.S. and receives $100,000 per year. Since 1983, inflation in

the U.S. has reduced his real earnings. From 1983 to 2000, inflation in the U.S.

was 63%. So, his real income (measured in 1983 US dollars) has decreased

from $100,000 in 1983 to: ($100,000/1.63) = $61,349 in 2000, a decrease of

38.7%.

Bruce, who lives in Australia, received US $100,000 in 1983, which was worth

A$110,800. In 2000, he also received US$100,000, which was worth A$179,900

(in 2000 Australian dollars). Because of Australian inflation (202% since 1983),

his real income in 2000 (measured in 1983 Australian dollars) was:

A$179,900/2.02 = A$89,059

Therefore, Bruce’s real income, measured in Australian dollars, has decreased

by 19.6%.

15. a. If the law of one price holds, then the bottle of Scotch will cost the same

anywhere, which implies that:

US$22.84 = S$69 ⇒US$1 = S$3.02

US$22.84 = 3240 roubles ⇒US$1 = 141.9 roubles

49

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

1983

1985

1987

1989

1991

1993

1995

1997

1999

Year

A$/US$

Nominal

Real

![Giáo trình Kế toán Trung cấp Tài chính Doanh nghiệp: [Hướng dẫn chi tiết/mới nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260526/alfredodistefano10/135x160/70231780288289.jpg)

![Bài tập Phân tích kinh doanh [chuẩn nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260513/hoacattuong2026/135x160/41481778835180.jpg)

%20--%3e%3cdefs%3e%3cstyle%3e%20.st0%20{%20fill:%20%23fff;%20}%20.st1%20{%20fill:%20%237800fa;%20}%20%3c/style%3e%3c/defs%3e%3cpath%20class='st1'%20d='M117.78,12.18H43.11c2.9,3.47,4.65,7.94,4.65,12.82,0,5.6-2.3,10.66-6.01,14.29h76.02l7.22-13.56-7.22-13.56Z'/%3e%3cg%3e%3cpath%20class='st0'%20d='M53.58,26.17h-.59v-1.46h.59v-4.96h2.83c1.78,0,2.67.94,2.67,2.82v5.76c0,1.87-.89,2.81-2.67,2.81h-2.83v-4.96ZM55.36,21.37v3.34h1.1v1.46h-1.1v3.34h1.01c.61,0,.91-.37.91-1.1v-5.93c0-.74-.3-1.1-.91-1.1h-1.01Z'/%3e%3cpath%20class='st0'%20d='M65.99,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM65.28,18.04c-.25.46-.51.77-.75.94-.21.15-.47.22-.79.22-.26,0-.57-.07-.92-.22l-.38-.15c-.14-.05-.26-.07-.37-.07-.3,0-.53.18-.71.54l-.91-.68c.25-.46.51-.77.75-.94.21-.14.48-.21.79-.21.26,0,.57.07.92.21l.38.15c.14.05.26.07.37.07.3,0,.53-.18.71-.54l.91.68ZM61.91,27.52h1.73l-.87-5.76-.87,5.76Z'/%3e%3cpath%20class='st0'%20d='M74.53,26.89v1.52c0,1.91-.89,2.86-2.67,2.86s-2.67-.95-2.67-2.86v-5.93c0-1.91.89-2.86,2.67-2.86s2.67.95,2.67,2.86v1.11h-1.69v-1.22c0-.75-.31-1.12-.93-1.12s-.93.37-.93,1.12v6.15c0,.74.31,1.11.93,1.11s.93-.37.93-1.11v-1.63h1.69Z'/%3e%3cpath%20class='st0'%20d='M81.4,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM75.9,19.2l1.52-1.91h1.71l1.51,1.91h-1.61l-.76-.95-.75.95h-1.61ZM77.32,27.52h1.73l-.87-5.76-.87,5.76ZM83.1,15.99l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M84.86,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM84.01,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M93.51,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM92.66,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M98.8,31.14h-1.79v-11.39h1.79v4.88h2.03v-4.88h1.83v11.39h-1.83v-4.88h-2.03v4.88Z'/%3e%3cpath%20class='st0'%20d='M105.36,24.55h2.46v1.62h-2.46v3.34h3.09v1.63h-4.88v-11.39h4.88v1.63h-3.09v3.18ZM108.17,17.29l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M112.2,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM111.35,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3c/g%3e%3ccircle%20class='st1'%20cx='25'%20cy='25'%20r='20'/%3e%3cpath%20class='st0'%20d='M32.78,19.27c2.92,0,4.43,2.55,5.28,5.33l.71,2.17c.14.38-.33.75-.71.75h-5.61c.19-.33.24-.71.09-1.08l-.75-2.45c-.43-1.32-.99-2.64-1.79-3.77.75-.57,1.65-.94,2.78-.94h0ZM25,18.38c3.25,0,4.9,2.78,5.89,5.89l.76,2.45c.14.42-.33.8-.8.8h-11.69c-.42,0-.94-.38-.8-.8l.75-2.45c.99-3.11,2.64-5.89,5.89-5.89h0ZM25,11.35c1.74,0,3.11,1.37,3.11,3.11s-1.37,3.11-3.11,3.11-3.11-1.41-3.11-3.11,1.41-3.11,3.11-3.11h0ZM17.27,19.27c1.08,0,1.98.38,2.73.94-.8,1.13-1.37,2.45-1.74,3.77l-.8,2.45c-.14.38-.05.75.09,1.08h-5.56c-.42,0-.9-.38-.75-.75l.71-2.17c.9-2.78,2.41-5.33,5.33-5.33h0ZM17.27,12.91c1.51,0,2.78,1.27,2.78,2.83s-1.27,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM32.78,12.91c1.56,0,2.78,1.27,2.78,2.83s-1.23,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM27.07,28.56v.09c0,.57-.24,1.08-.61,1.46h0v.05c-.38.33-.9.57-1.46.57s-1.08-.24-1.46-.61h0c-.38-.38-.61-.9-.61-1.46v-.09h1.41v.09c0,.19.05.38.19.47v.05c.09.09.28.19.47.19s.38-.09.47-.19v-.05c.14-.09.24-.28.24-.47t-.05-.09h1.41ZM30.99,28.56v.09c0,1.65-.66,3.16-1.74,4.24-1.08,1.08-2.59,1.79-4.24,1.79s-3.16-.71-4.24-1.79l-.05-.05c-1.04-1.08-1.7-2.55-1.7-4.2v-.09h1.41v.09c0,1.27.47,2.4,1.27,3.25h.05c.85.85,1.98,1.37,3.25,1.37s2.4-.52,3.25-1.37c.85-.8,1.37-1.98,1.37-3.25v-.09h1.37ZM34.99,28.56v.09c0,2.78-1.13,5.28-2.92,7.07-1.79,1.79-4.29,2.92-7.07,2.92s-5.23-1.13-7.07-2.92c-1.79-1.79-2.92-4.29-2.92-7.07v-.09h1.41v.09c0,2.4.94,4.53,2.5,6.08,1.56,1.56,3.72,2.5,6.08,2.5s4.52-.94,6.08-2.5c1.56-1.56,2.5-3.68,2.5-6.08v-.09h1.41Z'/%3e%3c/svg%3e)