http://www.iaeme.com/IJM/index.asp 152 editor@iaeme.com

International Journal of Management (IJM)

Volume 8, Issue 6, Nov–Dec 2017, pp. 152–162, Article ID: IJM_08_06_016

Available online at

http://www.iaeme.com/ijm/issues.asp?JType=IJM&VType=8&IType=6

Journal Impact Factor (2016): 8.1920 (Calculated by GISI) www.jifactor.com

ISSN Print: 0976-6502 and ISSN Online: 0976-6510

© IAEME Publication

WORKING CAPITAL MANAGEMENT AND

FIRM PROFITABILITY: A STUDY OF LISTED

COMPANIES IN INDIA

Arpita Naskar

Department of MBA, Student of Future Institute of Engineering and Management,

Sonarpur, Kolkata, India

Prasanta Guha

Department of MBA, Faculty of Future Institute of Engineering and Management,

Sonarpur, Kolkata, India

ABSTRACT

Financing decision of an entity bears relation with working capital management.

It is a part of short term financing. The study of corporate finance is also linked with

Working capital management. Thus, this study sought to examine the effect of working

capital management on profitability of select companies listed in BSE The study used

a sample of 53 companies. The study used secondary data for a period of 5 years from

2011 – 2015. The data have been analysed using the Pearson correlation and the

multivariate regression analysis. The study has revealed that the all components of

working capital namely Receivable days( RD), Payable days(PD), Inventory holding

periods ( ID), Current ratio ( CR) and Quick ratio ( QR) have strong impact on

profitability. Cash conversion cycle (CCC) is negatively related with the profitability,

Firm size is also linked with working capital. If firm size increases, the need of

working capital will be more. It has been found that the firm size has also significant

impact on EBIT but insignificant impact on ROA and ROE. Finally the study has

established a relation between working capital management and firm’s profitability.

Keyword head: Working capital management, Firm’s profitability, ROA, ROE, RD,

CCC

Cite this Article: Arpita Naskar and Prasanta Guha, Working Capital Management

and Firm Profitability: A Study of Listed Companies in India. International Journal of

Management, 8 (6), 2017, pp. 152–162.

http://www.iaeme.com/IJM/issues.asp?JType=IJM&VType=8&IType=6

1. INTRODUCTION

Many research has been conducted in the area of long term financing decisions viz.

investment decisions , capital structure and business valuation etc. In comparison to that

limited study has been extended in the field of working capital management. Working capital

Working Capital Management and Firm Profitability: A Study of Listed Companies in India

http://www.iaeme.com/IJM/index.asp 153 editor@iaeme.com

is the fund required to meet daily expenses in a business organization. It is the amount

invested in the current assets and can easily be converted into cash without changing the value

of the business (Mohanty, 2013). It can be expressed technically as excess of current assets

over current liabilities. Positive working capital reflects the capacity to pay short term

obligation while the negative working capital reflects the weakness of inability to pay the

same. Besides the negative working capital, excess is also not desirable. Insolvency may

cause due to inadequate working capital (Singh and Asress, 2010).

Working capital management ensures the proper balancing of different components say

debtors, receivable, cash balance, inventory, payables etc. The balance can be achieved by

minimizing the working capital requirement and maximizing the earning (Ganesan,2007).

Such balancing draws two concepts, liquidity and profitability. Liquidity gives strength to

meet short term obligation on the other hand firm’s ability to earn profit is reflected by

profitability quotient. It acts as a measure of firm performance. Effective working capital

management provides a firm to increase profitability along with the solution of optimum

liquidity (Uchenna et al., 2012).

2. LITERATURE REVIEW

Researchers have concentrated in the different areas of appropriate application of working

capital management. Working capital is just a fuel to a business named car. Extra penny

invested in the working capital would result to the decrease in value of the firm (Kieschnick et

al, (2006) . The prime question comes to the mind of the authors about the volume of working

capital. To understand the requirement of working capital , cash conversion cycle need to be

understood. This concept was first conceived by Richards and Laughlin (1980). Cash

conversion cycle ( CCC) is the summation of material procurement time, raw material

conversion period , inventory holding period and receivable days reduced by payable periods.

Raw materials conversion means to production time. More of production time will increase

CCC. More of finished goods holding period will cause to stretch the CCC. Similarly,

receivable days or periods refers to the time of goods sold on credit to collection from

customers. More the lengthy time to receive payments from debtors , more will be the CCC.

Payable days can be explained as the time to purchase the goods from suppliers to pay the

dues to suppliers. The management part lies in managing the time. Shorter the time period of

CCC or and increase in payable days , will require less amount of working capital. Increase in

payable days may apparently benefits the organization by arranging less amount of working

capital but in the long run it affects the goodwill of the organization.

Yogendrarajah and Thanabalasingam (n.d.) in their research revealed that firm’s

profitability can be increased by the effective inventory management. With reference to the

listed companies in Istambul , researchers found that the shareholders value can be increased

by reducing the accounts receivable period, accounts payable period and cash conversion

cycle (samiloglu and Akgun,2016).The same has been supported by Deloof (2003). Mansoori

and Muhammad (2012) also examined that the same fact in the context of Singapore. Using

OLS method their result revealed that the cash conversion cycle is negatively associated with

return on assets (ROA) where ROA is considered as a parameter of profitability.

Agha (2014) studied the same on a firm listed in Karachi stock exchange. The study

revealed that a firm can increase it’s profitability by minimizing the inventory turnover,

account receivables ratio and by decreasing creditors turnover ratios but there is no significant

effect of increasing or decreasing the current ration profitability. So, the results indicate that

through proper working capital management the company can increase it’s profitability. A

negative relationship has been prominent between debt and profitability of Indian firms in the

Arpita Naskar and Prasanta Guha

http://www.iaeme.com/IJM/index.asp 154 editor@iaeme.com

study of Chatterjee (2012). The results derived from this research signify that A firm is able to

raise it’s profits by diminishing the time period for the debtors and inventories so that the time

period for payables would increase. Discussing the same Makori and Jagongo (2013) find a

negative relationship between profitability and number of day’s accounts receivable and cash

conversion cycle, but a positive relationship between profitability and number of days of

inventory and number of day’s payable. Moreover, the financial leverage, sales growth,

current ratio and firm size also have significant effects on the firm’s profitability. Based on

the key findings from this study it has been concluded that the management of a firm can

create value for their shareholders by reducing the number of day’s accounts receivable

(Makori and Jagongo,2013). Similar results have been established by Elfani and Lois (2010);

Eljely (2004 ) and Jose (1996) have made the founding in their study that managers creates

value by reducing their volume of inventories and dues with the debtors and firm’s

profitability can be improved by shortening the cash conversion cycle.

The findings on the effect of working capital management and firm’s performance or

profitability of the researchers mentioned in the literature are quite similar. The author is also

interested to test the same varying with the companies and time span.

3. RESEARCH OBJECTIVES

The research objective is to study the relationship between profitability of the firm with the

working capital management. The specific objectives are as follows:

To study the impact of Working capital management of Indian firms listed in BSE

To observe the effect of accounts receivables, inventories holding periods, accounts payable

and cash conversion cycle on firm’s profitability

4. METHODOLOGY

Data and Sample Selection

The data used for the research have been obtained from the website www.arcadiastock.com

and individual website of the sample companies. Financial statements and annual reports have

been used for the study. The data comprising of 53 firms forty sectors listed in BSE have been

considered for study( see Table 1). A time period of 5 years with the span of 2011 to 2015 has

been taken for analysis. The name of the firms and sectors are given in the Table No.1.

Conceptual Framework

Independent variables:

An independent variable is the variable which the researcher has control over. In this study

the independent variable are Receivable days (RD),Inventory days(ID),Payable days(

PD),Cash conversion cycle ( CCC) ,Current ratio (CR), Quick ratio (QR), and Firm size or

LOGSALES .

Dependent variable

The profitability has been linked with dependent variables. The study has considered Earnings

before interest and tax (EBIT), Return on assets (ROA) and Return on equity(ROE) as

profitability indicator or dependent variable.

RD

Receivable days is the number of days that a customer invoice is outstanding before it is

collected. The point of measurement is to determine the effectiveness of a company’s credit

and collection efforts in allowing credit to reputable customers, as well as it’s ability to collect

cash from them. RD is calculated as ( Debtors+ Bills Receivable) / Net Sales x 3

Working Capital Management and Firm Profitability: A Study of Listed Companies in India

http://www.iaeme.com/IJM/index.asp 155 editor@iaeme.com

ID

Inventory days presents the days of holding the inventory. More and more holding of

inventory will be less of inventory turnover ratio. The inventory turnover ratio is an efficiency

ratio that shows how effectively inventory is managed by comparing cost of goods sold with

average inventory for a period. The inventory days are calculated as 365 / (Cost of goods sold

by average inventory).

PD

Accounts Payable Days is an accounting concept related to Accounts Payable. It is the length

of time it takes to clear all outstanding Accounts Payable. This is useful for determining how

efficient the company is at clearing whatever short-term account obligations it may have. PD

has been computed as summation of Sundry Creditors and Bills payable/ net sales x 365.

CCC

The cash conversion cycle (CCC) is a metric that expresses the length of time, in days, that it

takes for a company to convert resource inputs into cash flows. In other words, the cash

conversion cycle calculation measures how long cash is tied up in inventory before the

inventory is sold and cash is collected from customers. CCC is computed as RD+ID-PD.

CR

The current ratio is a financial ratio that measures whether or not a firm has enough resources

to pay its debts over the next 12 months. It compares a firm's current assets to

its current liabilities. It is considered as liquidity ratio. CR is calculated as current

assets/current liabilities.

QR

The quick ratio is a financial ratio used to gauge a company's liquidity. The quick ratio is also

known as the acid test ratio. It can be calculated as current assets – stock divided by current

liabilities.

LOG SALES

Size of the firm is linked with profitability. By the increase in size, earning of a firm

increases. The natural logarithm of sales (LOS) measures the growth of the firm. Logsales is

the natural logarithm of net sales.

EBIT

It is the amount of money that a company has earned after deducting the cost of goods

sold and operating expenses. This is used to see whether a company is making more than it

spends or is operating at a loss. The paper has used EBIT margin as a profitability variable.

ROA

Return on assets (ROA) is an indicator of how profitable a company is relative to its total

assets. ROA gives an idea as to how efficient management is at using its assets to generate. It

can be calculated as Net Income/Total assets .

ROE

Return on equity (ROE) is the amount of net income returned as a percentage

of shareholder’s equity. Return on equity measures a corporation's profitability by revealing

Arpita Naskar and Prasanta Guha

http://www.iaeme.com/IJM/index.asp 156 editor@iaeme.com

how much profit a company generates with the money shareholders have invested. ROE is

calculated as Net Income of the firm /Shareholder's Equity.

The analysis has been initiated with the descriptive statistics. To understand the relation

among the variables Pearson correlation statistics have been used. Further the study has been

proceeded to know the impact of independent variables on dependant variables and

multivariate regression analysis has been applied.

5. RESULTS AND DISCUSSIONS

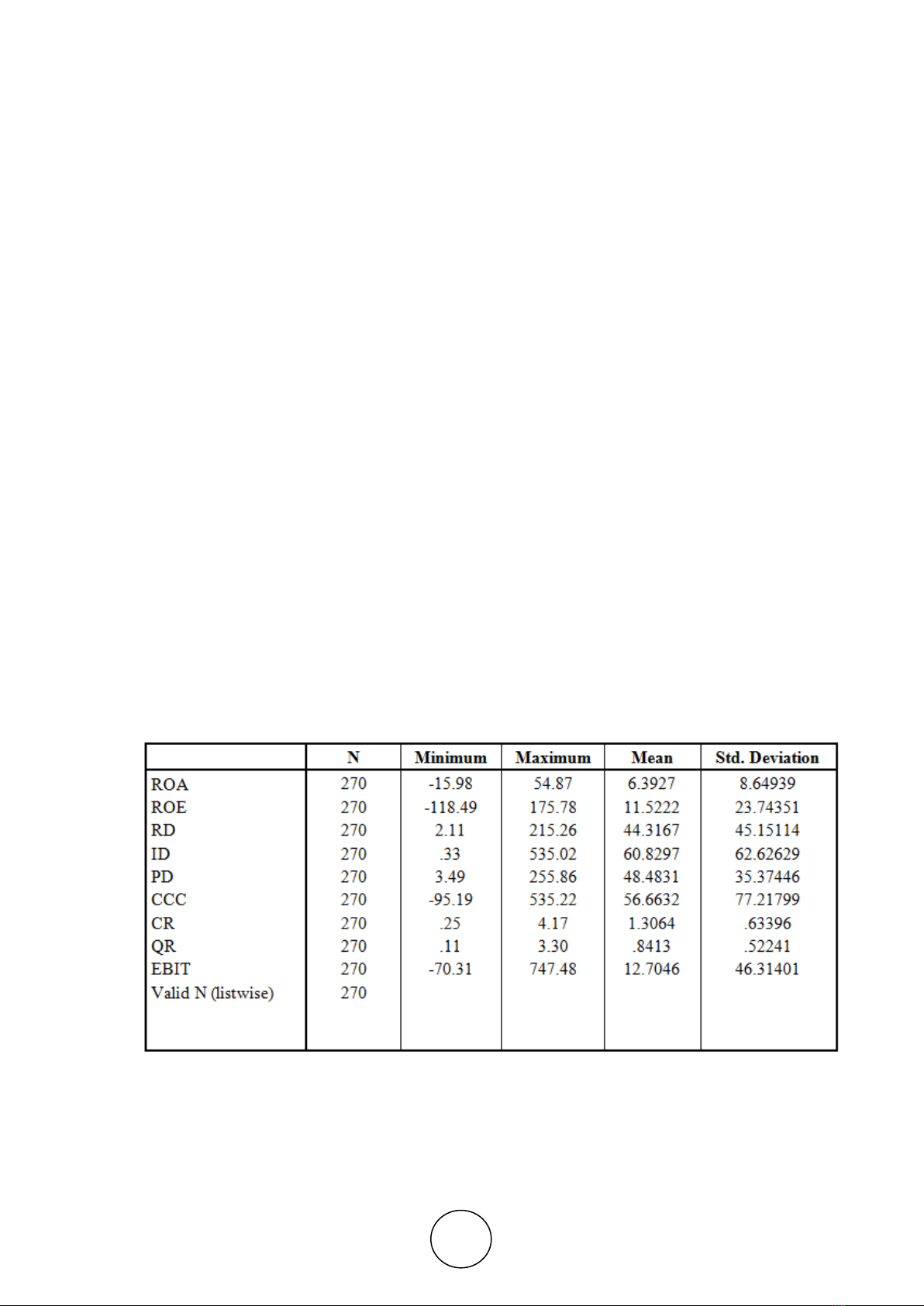

Refereeing to Table 2, the descriptive statistics of different variables applied in the research

have been presented. It presents maximum value, minimum value , mean and standard

deviation of 55 different companies for the span of 2011- 2015. Out of the total 270 nos of

observations mean value of ROA for all the industries is 6.39 with a maximum of 54.87 and a

minimum of -15.98. The standard deviation also shows a 8.64 of deviation from the mean.

The ROE has a maximum value of175.78, a minimum of -118.49 and a mean of 11.52

followed by a standard deviation of 27.74. Of the liquidity indicators firstly, the CCC has a

maximum of 535.22 days and a minimum of -95.19 days followed by a mean of 56.66 days

and 77.21days as standard deviation. Secondly, the CR shows a mean of 1.30:1 a maximum

value of 4.17:1 and a minimum value of .25:1. The standard deviation for CR is .63. Thirdly,

the ID shows a mean of 60.82 days with a maximum of 535.22 days and a minimum of .33

days. The standard deviation for the ID is 62.62. Fourthly, the RD has a maximum value of

215.26 days, a minimum of 2.11 days and a mean of 44.31 days followed by a standard

deviation of 45.15. Fifthly, the PD has a maximum of 255.86 days, a minimum of 3.49 days

and a mean of 48.48 days with a standard deviation of 35.37. Sixthly, the QR has .11:1 as

minimum,3.30:1 as maximum,.84:1 as mean and .52 as standard deviation. Finally, EBIT has

a mean of 12.70 with a maximum of 747.48, minimum of -70.31 and a standard deviation of

46.31.

Table 2 Descriptive Statistics

Table 3 presents the correlation to understand the interrelations between variables. Being a

measure of profitability, ROA is negatively influenced by CCC and it has statistically

significant impact. Similarly ROE and EBIT are negatively correlated (Deloof ,2003).

RD or receivable days and ID or inventory holding periods have been found as negative

correlated with profitability supported by ROA, ROE. It reflects if receivable days and or

![Giáo trình Kế toán Trung cấp Tài chính Doanh nghiệp: [Hướng dẫn chi tiết/mới nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260526/alfredodistefano10/135x160/70231780288289.jpg)

![Bài tập Phân tích kinh doanh [chuẩn nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260513/hoacattuong2026/135x160/41481778835180.jpg)

%20--%3e%3cdefs%3e%3cstyle%3e%20.st0%20{%20fill:%20%23fff;%20}%20.st1%20{%20fill:%20%237800fa;%20}%20%3c/style%3e%3c/defs%3e%3cpath%20class='st1'%20d='M117.78,12.18H43.11c2.9,3.47,4.65,7.94,4.65,12.82,0,5.6-2.3,10.66-6.01,14.29h76.02l7.22-13.56-7.22-13.56Z'/%3e%3cg%3e%3cpath%20class='st0'%20d='M53.58,26.17h-.59v-1.46h.59v-4.96h2.83c1.78,0,2.67.94,2.67,2.82v5.76c0,1.87-.89,2.81-2.67,2.81h-2.83v-4.96ZM55.36,21.37v3.34h1.1v1.46h-1.1v3.34h1.01c.61,0,.91-.37.91-1.1v-5.93c0-.74-.3-1.1-.91-1.1h-1.01Z'/%3e%3cpath%20class='st0'%20d='M65.99,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM65.28,18.04c-.25.46-.51.77-.75.94-.21.15-.47.22-.79.22-.26,0-.57-.07-.92-.22l-.38-.15c-.14-.05-.26-.07-.37-.07-.3,0-.53.18-.71.54l-.91-.68c.25-.46.51-.77.75-.94.21-.14.48-.21.79-.21.26,0,.57.07.92.21l.38.15c.14.05.26.07.37.07.3,0,.53-.18.71-.54l.91.68ZM61.91,27.52h1.73l-.87-5.76-.87,5.76Z'/%3e%3cpath%20class='st0'%20d='M74.53,26.89v1.52c0,1.91-.89,2.86-2.67,2.86s-2.67-.95-2.67-2.86v-5.93c0-1.91.89-2.86,2.67-2.86s2.67.95,2.67,2.86v1.11h-1.69v-1.22c0-.75-.31-1.12-.93-1.12s-.93.37-.93,1.12v6.15c0,.74.31,1.11.93,1.11s.93-.37.93-1.11v-1.63h1.69Z'/%3e%3cpath%20class='st0'%20d='M81.4,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM75.9,19.2l1.52-1.91h1.71l1.51,1.91h-1.61l-.76-.95-.75.95h-1.61ZM77.32,27.52h1.73l-.87-5.76-.87,5.76ZM83.1,15.99l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M84.86,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM84.01,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M93.51,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM92.66,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M98.8,31.14h-1.79v-11.39h1.79v4.88h2.03v-4.88h1.83v11.39h-1.83v-4.88h-2.03v4.88Z'/%3e%3cpath%20class='st0'%20d='M105.36,24.55h2.46v1.62h-2.46v3.34h3.09v1.63h-4.88v-11.39h4.88v1.63h-3.09v3.18ZM108.17,17.29l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M112.2,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM111.35,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3c/g%3e%3ccircle%20class='st1'%20cx='25'%20cy='25'%20r='20'/%3e%3cpath%20class='st0'%20d='M32.78,19.27c2.92,0,4.43,2.55,5.28,5.33l.71,2.17c.14.38-.33.75-.71.75h-5.61c.19-.33.24-.71.09-1.08l-.75-2.45c-.43-1.32-.99-2.64-1.79-3.77.75-.57,1.65-.94,2.78-.94h0ZM25,18.38c3.25,0,4.9,2.78,5.89,5.89l.76,2.45c.14.42-.33.8-.8.8h-11.69c-.42,0-.94-.38-.8-.8l.75-2.45c.99-3.11,2.64-5.89,5.89-5.89h0ZM25,11.35c1.74,0,3.11,1.37,3.11,3.11s-1.37,3.11-3.11,3.11-3.11-1.41-3.11-3.11,1.41-3.11,3.11-3.11h0ZM17.27,19.27c1.08,0,1.98.38,2.73.94-.8,1.13-1.37,2.45-1.74,3.77l-.8,2.45c-.14.38-.05.75.09,1.08h-5.56c-.42,0-.9-.38-.75-.75l.71-2.17c.9-2.78,2.41-5.33,5.33-5.33h0ZM17.27,12.91c1.51,0,2.78,1.27,2.78,2.83s-1.27,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM32.78,12.91c1.56,0,2.78,1.27,2.78,2.83s-1.23,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM27.07,28.56v.09c0,.57-.24,1.08-.61,1.46h0v.05c-.38.33-.9.57-1.46.57s-1.08-.24-1.46-.61h0c-.38-.38-.61-.9-.61-1.46v-.09h1.41v.09c0,.19.05.38.19.47v.05c.09.09.28.19.47.19s.38-.09.47-.19v-.05c.14-.09.24-.28.24-.47t-.05-.09h1.41ZM30.99,28.56v.09c0,1.65-.66,3.16-1.74,4.24-1.08,1.08-2.59,1.79-4.24,1.79s-3.16-.71-4.24-1.79l-.05-.05c-1.04-1.08-1.7-2.55-1.7-4.2v-.09h1.41v.09c0,1.27.47,2.4,1.27,3.25h.05c.85.85,1.98,1.37,3.25,1.37s2.4-.52,3.25-1.37c.85-.8,1.37-1.98,1.37-3.25v-.09h1.37ZM34.99,28.56v.09c0,2.78-1.13,5.28-2.92,7.07-1.79,1.79-4.29,2.92-7.07,2.92s-5.23-1.13-7.07-2.92c-1.79-1.79-2.92-4.29-2.92-7.07v-.09h1.41v.09c0,2.4.94,4.53,2.5,6.08,1.56,1.56,3.72,2.5,6.08,2.5s4.52-.94,6.08-2.5c1.56-1.56,2.5-3.68,2.5-6.08v-.09h1.41Z'/%3e%3c/svg%3e)