23

© Học viện Ngân hàng

ISSN 3030 - 4199

Tạp chí Kinh tế - Luật & Ngân hàng

Số 270- Năm thứ 26 (11)- Tháng 10. 2024

Mối quan hệ giữa Bitcoin và thị trường ngoại hối

ASEAN-6

Ngày nhận: 07/03/2024 Ngày nhận bản sửa: 29/06/2024 Ngày duyệt đăng: 05/07/2024

Tóm tắt: Nghiên cứu khám phá tương quan giữa giá Bitcoin và thị trường

ngoại hối các nước ASEAN-6, bao gồm: Singapore, Việt Nam, Malaysia, Thái

Lan, Indonesia, và Philippines ở giai đoạn 2018 đến 2023. Chúng tôi sử dụng

mô hình chỉ số lan tỏa-SPI kết hợp với kiểm định nhân quả Granger dạng phổ.

Kết quả cho thấy giá Bitcoin và thị trường ngoại hối ASEAN-6 biến động theo

thời gian và tồn tại mối quan hệ về giá giữa các thị trường, tăng cao trong

đại dịch COVID-19, khủng hoảng năng lượng Châu Âu và lạm phát toàn cầu

năm 2023. Chỉ số lan tỏa về giá tăng cao và chạm đỉnh vào thời điểm đại dịch

Relationship between Bitcoin and ASEAN-6 foreign exchange rate markets

Abstract: This study highlights the nexus between Bitcoin and foreign exchange markets in ASEAN-6

countries, including Vietnam, Thailand, Singapore, Indonesia, Malaysia, and Philippines, from 2018 to 2023,

utilizing the spillover index and the spectral Granger causality test. The findings indicate that Bitcoin and

the foreign exchange markets co-moved over time, and the connectedness between the markets increased

significantly during the COVID-19 pandemic, the European energy crisis, and global inflation in 2023. The

total spillover index reaches 13.4%, suggesting the connection between market returns is relatively low.

Indonesia, Thailand, Vietnam, and Thailand are receivers, while Bitcoin, Malaysia, the Philippines, and

Singapore are transmitters. The results of the Granger test illustrate that there exists a one-way causality

running from Bitcoin to Malaysia, Vietnam, Thailand, from the Philippines to Bitcoin, and a two-way

association between Indonesia and Bitcoin in the medium and long term and Singapore and Bitcoin in the

long term. These results are valuable information for investors, stakeholders, and policymakers to stabilize

the foreign exchange market.

Keywords: ASEAN-6, Granger causality, Spillover Index, Foreign exchange rate, Bitcoin

Doi: 10.59276/JELB.2024.10.2687

Ngo, Thai Hung1, Le, Vu Ngoc Nga2, Tran, Tien Thao Nguyen3, Nguyen, Thi Ngoc Chau4, Huynh, Ngoc My

Huong5, Lam, Thanh Thuy6

Email: ngothai.hung@gmail.com1, lenga35.2003@gmail.com2, thaonguyen14032003@gmail.com3,

ngocchau2003lk@gmail.com4, myhuong2020.hcm@gmail.com5, 96lamthanhthuy1718@gmail.com6

Organization of all: University of Finance and Marketing, Vietnam

Ngô Thái Hưng1, Lê Vũ Ngọc Nga2, Trần Tiến Thảo Nguyên3, Nguyễn Thị Ngọc Châu4,

Huỳnh Ngọc Mỹ Hương5, Lâm Thanh Thủy6

Đại học Tài Chính-Marketing, Việt Nam

Mối quan hệ giữa Bitcoin và thị trường ngoại hối ASEAN-6

24 Tạp chí Kinh tế - Luật & Ngân hàng- Số 270- Năm thứ 26 (11)- Tháng 10. 2024

1. Giới thiệu

Kể từ khi được giao dịch lần đầu tiên tại

sàn giao dịch New Liberty Standard vào

năm 2009, Bitcoin đã nhanh chóng được

sử dụng như một phương tiện trao đổi vào

năm 2013 (Oh và Nguyen, 2018). Tuy

nhiên, hầu hết nhà nghiên cứu đều đưa ra

quan điểm cảnh báo rằng thị trường Bitcoin

là một bong bóng, nó sẽ vỡ trong tương

lai và lan truyền rủi ro đến các thị trường

khác (Cheah và Fry, 2015). Nghiên cứu về

sự tác động của tiền điện tử nói chung và

các thị trường khác rất hữu dụng cho các

nhà hoạch định chính sách để cải thiện hệ

thống pháp lý ở các nền kinh tế khác nhau

(Corbet, 2018). Trong đó, Bitcoin là chủ đề

thu hút nhiều nghiên cứu về sự tác động

của nó với các loại tài sản khác (Demir và

cộng sự, 2018).

Sự lan tỏa biến động từ thị trường tiền điện

tử sang tài sản tài chính ngày càng phổ biến

trong các nghiên cứu khoa học thời gian

gần đây (Kamal và Hassan, 2022; Naeem

và Karim, 2021). Một số nghiên cứu đã

cho thấy Bitcoin không được xem là tài

sản trú ẩn an toàn vì sự biến động liên tục

về giá của nó (Rahma và cộng sự, 2021)

và Bitcoin không tác động đến các loại

tài sản tài chính khác (Adel Benhamed và

cộng sự, 2023). Tuy nhiên, một số nghiên

cứu khác chỉ ra rằng, Bitcoin được sử dụng

như là một đồng tiền phòng ngừa rủi ro bởi

các nhà đầu tư tiền tệ (Urquhart và Zhang,

2019) và Bitcoin có mối tương quan tích

cực với các tài sản tài chính khác (Jerina và

Mohamad, 2022).

Trong khi phần lớn các đề tài nghiên cứu

tập trung vào mối quan hệ giữa tiền điện

tử và các tài sản khác thì sự phụ thuộc lẫn

nhau giữa tiền điện tử và thị trường ngoại

hối vẫn chưa có nhiều giải thích thỏa đáng

(Baumöhl, 2019; Kristjanpoller và Bouri,

2019). So với các thị trường tài chính khác,

một số đặc điểm khác biệt của thị trường

ngoại hối là khả năng thu hút các nhà đầu

tư và góp phần giúp các quốc gia trên thế

giới kết nối với nhau (Haiying Wang và

cộng sự, 2021). Lịch sử nghiên cứu đã

có nhiều tư liệu khai thác tác động của

Bitcoin đến thị trường ngoại hối của các

nước lớn mạnh, như BenSaïda (2023), họ

đưa ra kết luận nghiên cứu rằng tác động

của Bitcoin lên các loại tiền ở hai nhóm

quốc gia: G7 và BRICS là mối tương quan

âm. Ngược lại, nghiên cứu về tác động của

Bitcoin lên thị trường ngoại hối các nước

đang phát triển thuộc ASEAN-6 còn chưa

phổ biến và ít được đề cập đến. Thị trường

ngoại hối ASEAN-6 bao gồm 6 nước (Việt

COVID-19. Tổng chỉ số lan tỏa đạt 13,4%, nghĩa là sự tương quan giữa các thị

trường tương đối thấp. Hơn nữa, Indonesia, Thái Lan, Việt Nam, với Thái Lan

là thị trường Nhận, trong khi đó, Bitcoin, Malaysia, Philippines và Singapore là

thị trường Truyền. Kết quả kiểm định Granger cho biết tồn tại mối quan hệ một

chiều từ Bitcoin đến Malaysia, Việt Nam, Thái Lan, từ Philippines đến Bitcoin,

và mối quan hệ hai chiều giữa Indonesia và Bitcoin trong trung hạn và dài hạn,

Singapore và Bitcoin trong dài hạn. Kết quả nghiên cứu là kênh thông tin cần

thiết cho các chuyên gia hoạch định chính sách và chủ thể tham gia đầu tư góp

phần ổn định thị trường ngoại hối.

Từ khóa: ASEAN-6, Kiểm định nhân quả Granger dạng phổ, Chỉ số lan toả, Thị

trường ngoại hối, Bitcoin

NGÔ THÁI HƯNG - LÊ VŨ NGỌC NGA - TRẦN TIẾN THẢO NGUYÊN -

NGUYỄN THỊ NGỌC CHÂU - HUỲNH NGỌC MỸ HƯƠNG - LÂM THANH THỦY

25

Số 270- Năm thứ 26 (11)- Tháng 10. 2024- Tạp chí Kinh tế - Luật & Ngân hàng

Nam, Thái Lan, Singapore, Indonesia,

Malaysia và Philippines). Đây là nhóm

các quốc gia có tốc độ tăng trưởng kinh tế

nhanh chóng trong khu vực Đông Nam Á.

Hơn nữa, ASEAN-6 là một thị trường sôi

động và là một khu vực để đầu tư với tốc

độ tăng trưởng kinh tế nhanh chóng. Một

chỉ tiêu quan trọng trong sự thành công

của phát triển kinh tế là quản trị rủi ro

(Sethapramote, 2015). Do đó, nghiên cứu

hiện tại khám phá mối quan hệ của Bitcoin

và thị trường ngoại hối các quốc gia thuộc

khối ASEAN-6 bằng mô hình chỉ số giá

lan toả-SPI và kiểm định nhân quả Granger

dạng phổ, nhằm chỉ ra ảnh hưởng của giá

Bitcoin đến thị trường ngoại hối của các

nước ASEAN-6 và phân tích, đánh giá

tính chặt chẽ trong quan hệ của Bitcoin và

các thị trường ngoại hối này. Từ đó, nhóm

nghiên cứu gợi ý một vài chính sách giúp

ổn định thị trường ngoại hối ASEAN-6.

Nghiên cứu đóng góp lý thuyết thực

nghiệm về sự lan tỏa giá giữa Bitcoin và

các thị trường ngoại hối ASEAN-6 trong

giai đoạn từ 2018-2023. Đặc biệt, nghiên

cứu hiện tại sử dụng phương pháp chỉ số

lan tỏa-SPI được phát triển bởi Diebold and

Yilmaz (2014), cung cấp thông tin lan tỏa

về giá của các thị trường được nghiên cứu

theo thời gian dưới hai góc độ “Truyền và

Nhận”, từ đó đánh giá mức độ ảnh hưởng

biến động của giá Bitcoin lên thị trường

ngoại hối của các quốc gia ASEAN-6. Hơn

nữa, kiểm định nhân quả Granger dạng phổ

phát triển bởi Breitung và Candelon (2006)

được áp dụng trong nghiên cứu này nhằm

chứng minh tồn tại mối quan hệ hai chiều

giữa các thị trường trong các giai đoạn

khác nhau: ngắn hạn, trung hạn và dài hạn.

Kết quả đạt được cung cấp một số hàm ý

quan trọng cho nhà đầu tư và nhà làm chính

sách ở các nước ASEAN-6 trong giai đoạn

khủng hoảng. Vì vậy, nghiên cứu hiện tại

mang lại điểm khác biệt và đóng góp kịp

thời, làm tiền đề tham khảo cho các nghiên

cứu sau này.

2. Tổng quan nghiên cứu

Bitcoin là một loại tiền điện tử được tạo ra

bởi Satoshi Nakamoto từ năm 2008. Kể từ

khi được ra mắt đến nay, Bitcoin đã trải qua

nhiều giai đoạn phát triển vượt bậc để trở

thành một trong những loại tiền điện tử có

giá trị lớn. Chính vì vậy, mối liên hệ giữa

Bitcoin và các thị trường tài chính nhận

được nhiều sự quan tâm của các nhà đầu tư

trên phạm vi toàn cầu (Ozyesil, 2019). Đã

có nhiều kết luận nghiên cứu trước đây cho

thấy Bitcoin không ảnh hưởng tới tỷ giá

hối đoái của các nước khác. Chẳng hạn như

Nan và Kaizoji (2019) nghiên cứu tỷ giá

của đồng Bitcoin so với cặp tỷ giá đồng Đô

la Mỹ và đồng Euro, kết quả nghiên cứu

đã chỉ ra rằng Bitcoin không có mối tương

quan với USD/EUR. Bên cạnh đó, Drożd

và cộng sự (2019) phân tích về mối tương

quan giữa BIT, ETH, EUR, USD và đưa

ra kết quả cho thấy BIT, ETH, EUR, USD

không ảnh hưởng đến tỷ giá của USD,

EUR, USD, EUR, ETH. Ozyesil (2019)

phân tích sự tương tác giữa Bitcoin và tỷ

giá hối đoái USD/EUR, sau đó đưa ra kết

luận rằng giá của Bitcoin và Euro không

bị ảnh hưởng bởi đồng Đô la Mỹ. Đa số,

các nghiên cứu về tác động của Bitcoin lên

thị trường ngoại hối được thực hiện ở các

nước đã phát triển, tuy nhiên còn hạn chế ở

các nước Châu Á.

Gillaizeau và cộng sự (2019) quan sát về

sự biến động của giá Bitcoin đối với thị

trường ngoại hối BIT/USD, và đưa ra kết

quả rằng giá BIT tác động mạnh đến BIT/

USD. Tarasova và cộng sự (2020) dự báo

tỷ giá hối đoái của các loại tiền điện tử

BIT, USD, CL, XAU và đã đưa ra kết quả

cho thấy chiến tranh thương mại của Hoa

Kỳ với Trung Quốc ảnh hưởng đến tỷ giá

Mối quan hệ giữa Bitcoin và thị trường ngoại hối ASEAN-6

26 Tạp chí Kinh tế - Luật & Ngân hàng- Số 270- Năm thứ 26 (11)- Tháng 10. 2024

hối đoái của Bitcoin. Drożdż và cộng sự

(2020) kiểm định biến động của thị trường

tiền điện tử CAD, JPY, CHF, CL, XAU đối

với tỷ giá hối đoái BIT/USDT, ETH/USDT

và đã đưa ra các bằng chứng cho thấy BIT/

USDT, ETH/USDT tác động mạnh đến

CAD, JPY, CHF.

Ở những năm gần đây, Park Sangjin và

cộng sự (2021) đã phân tích mối quan hệ

giữa Bitcoin và tài sản tài chính (trái phiếu

Chính Phủ, thị trường chứng khoán và tỉ

giá hối đoái). Cuối cùng, họ đưa ra dẫn

chứng chứng minh Bitcoin phản ứng mạnh

mẽ với tỷ giá hối đoái của các thị trường

phát triển hơn là so với các thị trường mới

nổi. Trong cùng khoảng thời gian này,

Palazzi và cộng sự (2021) nghiên cứu về

mối quan hệ giữa Bitcoin và các đồng tiền

khác như: EUR, GBP, CHF, RMB, JPY,

RUB. Kết quả nhận định Bitcoin không có

mối tương quan với sáu loại tiền tệ: Euro,

bảng Anh, Franc Thụy Sĩ, Nhân dân tệ

Trung Quốc, Yên Nhật và Rúp Nga. Tuy

vậy, Bitcoin không được coi là nơi trú ẩn

an toàn do sự biến động về giá của nó. Đến

năm 2022, Khôi và Hưng (2022) nghiên

cứu về tác động của Bitcoin đến thị trường

chứng khoán các nước ASEAN-6. Kết quả

cho rằng Bitcoin có tác động bất đối xứng

đến các thị trường chứng khoán ASEAN-6

và tác động này thay đổi theo điều kiện thị

trường. Mallick và Mallik (2023) nghiên

cứu về mối quan hệ giữa Bitcoin và tỷ giá

hối đoái của Ấn Độ bằng các mô hình kinh

tế lượng truyền thống. Kết quả cho thấy

không có bất kỳ mối quan hệ quan trọng

nào giữa Bitcoin với tỷ giá hối đoái trên

thị trường ngoại hối Ấn Độ. Trước đó,

COVID-19 đã gây ra khủng hoảng kinh tế

trên toàn cầu, và ảnh hưởng của đại dịch lên

Bitcoin và thị trường ngoại hối trở thành

chủ đề cấp thiết, thu hút nhiều sự quan tâm

của các nhà đầu tư. Các bằng chứng về sự

thay đổi của Bitcoin đối với đồng Đô la

Mỹ (USD) trong giai đoạn trước và trong

thời điểm bùng phát đại dịch COVID-19 đã

được Zitis cùng cộng sự (2023) đưa ra gần

đây. Kết quả chỉ ra Bitcoin tác động đáng

kể đến USD trong giai đoạn COVID-19.

BenSaïda (2023) nghiên cứu về Bitcoin và

các loại tiền pháp định ở hai nhóm quốc

gia: G7 và BRICS trong thời kỳ đại dịch

COVID-19 và chiến tranh Nga-Ukraine,

kết quả cho thấy Bitcoin có mối tương

quan dương đối với các loại tiền ở hai

nhóm quốc gia G7 và BRICS.

Bogdan Andrei Dumitrescu và cộng sự

(2023) đã phân tích về ảnh hưởng của sự

biến động giá Bitcoin đến tỷ giá hối đoái

của các loại tiền tệ BGN, HRK, CZK,

HUF, NOK, PLN, RON, SEK, CHF. Bằng

cách sử dụng phương pháp hồi quy phân vị

(kết quả cho thấy giá Bitcoin có mối quan

hệ đồng biến với giá của các loại tiền tệ

trên. Chikobvu và Ndlovu (2023) nghiên

cứu về việc ước tính rủi ro về hai tỷ giá hối

đoái của Bitcoin đối với Đô la Mỹ (BIT/

USD) và đồng Rand Nam Phi đối với Đô

la Mỹ (ZAR/USD). Bằng cách sử dụng mô

hình GEVD, kết luận là BIT/USD rủi ro

hơn ZAR/USD.

Dựa vào những khảo lược trên, nghiên cứu

hiện tại đánh giá tác động của Bitcoin đến thị

trường tỷ giá các nước ASEAN-6. Nghiên

cứu này khác biệt với các nghiên cứu trước

đây bao gồm: (1) chúng tôi tập trung vào

thị trường ngoại hối các nước ASEAN-6

và khám phá mối liên hệ của chúng với thị

trường Bitcoin theo thời gian và trên các

miền tần số khác nhau (2) nghiên cứu này sử

dụng mô hình chỉ số lan tỏa bằng cách kết

hợp tỷ suất sinh lời của Bitcoin và tỷ giá hối

đoái thuộc các quốc gia ASEAN-6. Theo

khảo sát của chúng tôi, đây là bài báo đầu

tiên kiểm tra sự kết dính cả hai thị trường

theo thời gian để bộc lộ toàn diện các cú

sốc Bitcoin đến các thị trường tỷ giá khác

nhau (3) nghiên cứu hiện tại cũng nêu bật

NGÔ THÁI HƯNG - LÊ VŨ NGỌC NGA - TRẦN TIẾN THẢO NGUYÊN -

NGUYỄN THỊ NGỌC CHÂU - HUỲNH NGỌC MỸ HƯƠNG - LÂM THANH THỦY

27

Số 270- Năm thứ 26 (11)- Tháng 10. 2024- Tạp chí Kinh tế - Luật & Ngân hàng

mối quan hệ hai chiều giữa hai thị trường

này trên từng miền tần số khác nhau, qua đó

cung cấp thông tin quan trọng cho nhà đầu

tư và người tham gia thị trường.

3. Phương pháp nghiên cứu

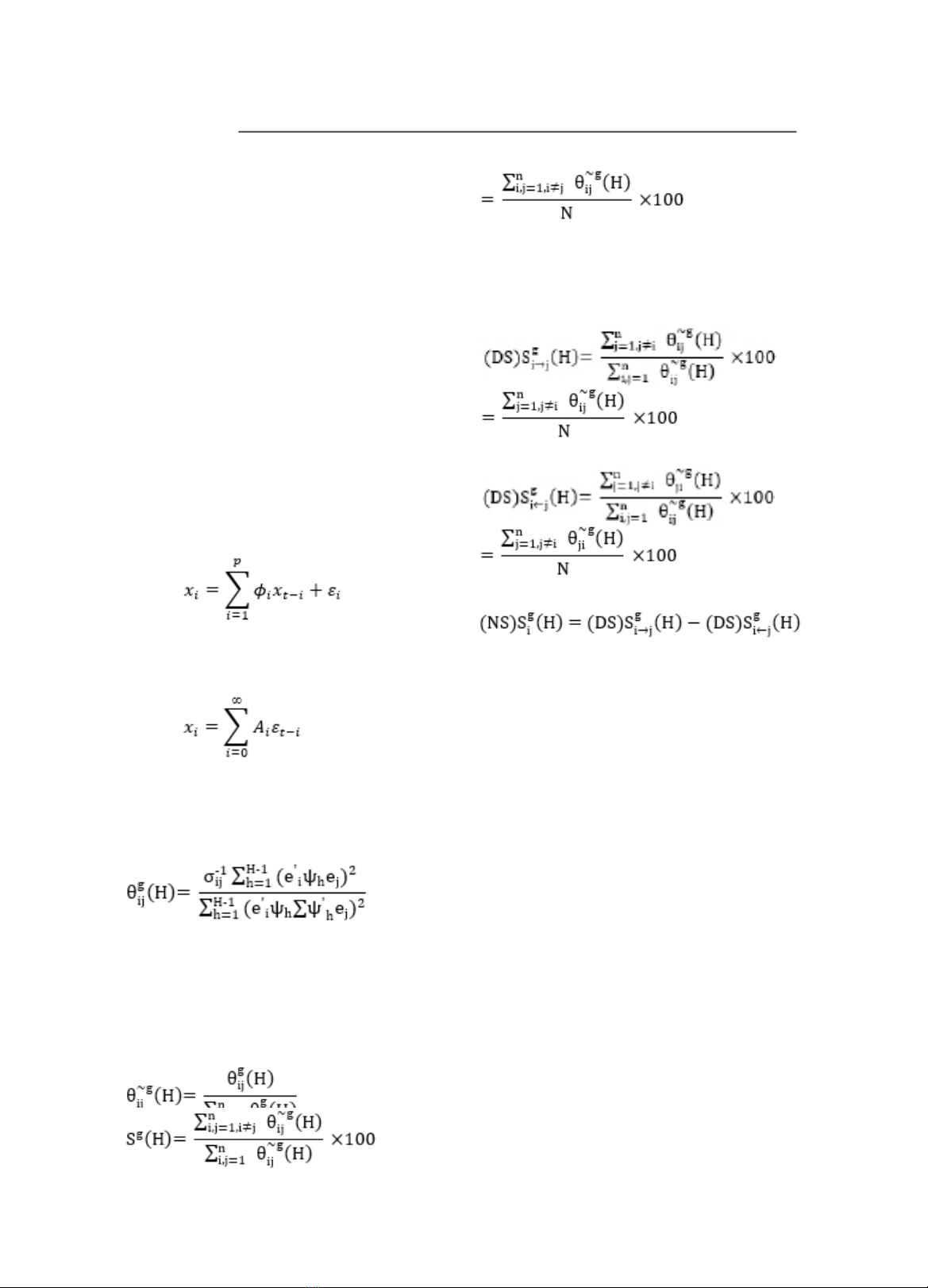

3.1. Chỉ số lan toả

Chỉ số lan toả (Spillover Index-SPI) lần

đầu được đề xuất trong nghiên cứu của

Diebold and Yilmaz (2009). SPI dùng để

đo lường mức độ kết nối giữa các chuỗi

thời gian dựa trên kết quả phân rã phương

sai của mô hình cơ bản.

Quá trình VAR (p) của nghiên cứu hiện tại

như sau:

(1)

DY được xây dựng trên khung mô hình

(VAR) bằng cách sử dụng trung bình trượt

như sau:

(2)

Trong đó, Ai là ma trận hệ số cấp N x N

được ước lượng như sau:

Ai = øiAi-1 + ø2Ai-2 + ... + øpAi-p với A0 = In

Phương sai sai số dự báo H được viết như sau:

(3)

Trong đó, Ʃ là ma trận phương sai sai số

ε, σij là độ lệch chuẩn của sai số thị trường

(Trung, 2024).

Phân tách phương sai ma trận H được hiển

thị dưới dạng:

(4)

Hiệu ứng lan tỏa tổng thể:

=

(5)

Chiều lan tỏa được phân loại thành

“Truyền” và “Nhận”.

Sự lan tỏa định hướng “Truyền” được tính

như sau:

(6)

Và sự lan tỏa định hướng “Nhận”:

(7)

Mức độ lan tỏa ròng như sau: (8)

3.2. Kiểm định nhân quả Granger dạng phổ

Việc kiểm định nhân quả dạng phổ, được

Breitung và Candelon (2006) giới thiệu,

nhằm xác định mối quan hệ hai chiều giữa

Xt , Yt tại từng miền tần số của chuỗi thời

gian. Điều kiện tiên quyết cho quá trình

kiểm định này đó là các chuỗi thời gian

phải là chuỗi dừng.

Đặt Zt = (Xt, Yt)’. Mô hình VAR(p) của Zt

như sau:

(I2 − A1L - ... - ApLp)Zt = εt (9)

Trong đó,

I2 : ma trận đơn vị cấp 2

Ai : ma trận hệ số cấp 2x2 của độ trễ i với

i =1, 2, 3,…p

L: toán tử lùi;

εt = (ε1t, ε2t)' : vecto sai số, trong đó ε1t, ε2t

là các chuỗi nhiễu trắng.

Biến đổi mô hình (9) thành dạng vectơ

trung bình trượt như sau:

Zt = ø(L)εt (10)

![Tỷ giá hối đoái: Tóm tắt kiến thức cơ bản [chuẩn SEO]](https://cdn.tailieu.vn/images/document/thumbnail/2021/20210816/buidangnhat/135x160/8821629082845.jpg)

![Tỷ giá hối đoái: Tài liệu [mới nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2014/20140523/duongxuan92/135x160/1681600_167.jpg)

![Đề thi Tài chính quốc tế kết thúc học phần: Tổng hợp [năm]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260310/hoatudang2026/135x160/36971773373442.jpg)