What do we need to get right

next time for a sustainable

property market in Vietnam?

Presented by:

Marc Townsend

Managing Director

Monday 21st September 2009

CB RICHARD ELLIS VIETNAM

2Where are we going? What have we learned? |September 2009

Risks

-Inflation

-Infrastructure

-Transparency

-The past was too good to give up

-NPLs

-Valuations

-Capital gains tax issues on the transfer of property

-Speculation is so easy

-Land clearance and tender and auction process

CB RICHARD ELLIS VIETNAM

3Where are we going? What have we learned? |September 2009

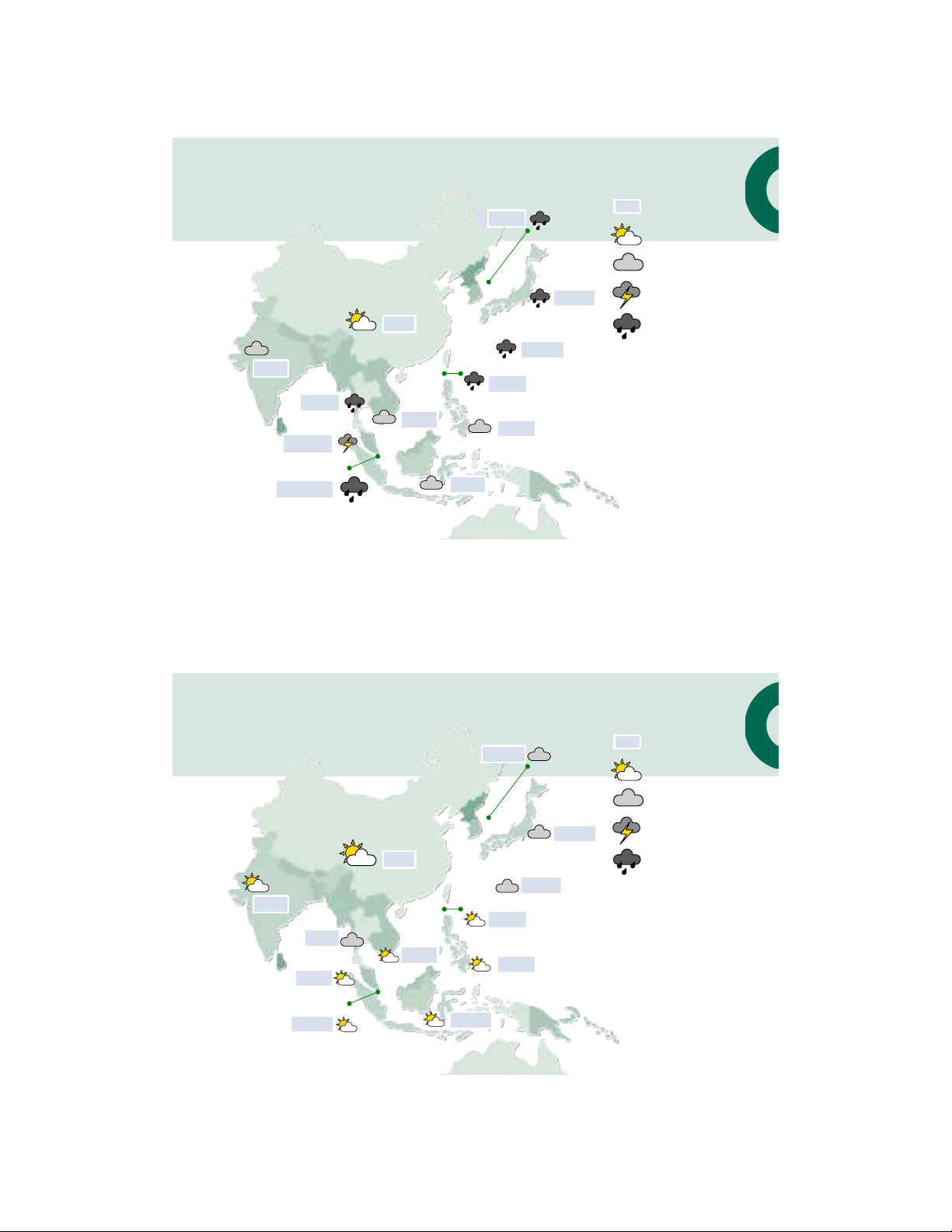

Asia economic outlook - 2009

Clouds over growth but

positive prospect

Clouds over growth and

dimmer prospect

Recent deterioration and

uncertain outlook

Continued deterioration

GDP growth

CHINA

SOUTH

KOREA

JAPAN

TAIWAN

HONG

KONG

PHILLIPPINES

VIETNAM

THAILAND

INDIA

MALAYSIA

SINGAPORE INDONESIA

6.5%

3.5%

-3.1%

1.4%

-2.5%

-6.5% 2.8%

-5.6%

-2.5%

-3.1%

-5.3%

6.0%

Source: IMA (April 2009)

CB RICHARD ELLIS VIETNAM

4Where are we going? What have we learned? |September 2009

Asia economic outlook - 2010

Clouds over growth but

positive prospect

Clouds over growth and

dimmer prospect

Recent deterioration and

uncertain outlook

Continued deterioration

GDP growth

Source: IMA (April 2009)

CHINA

SOUTH

KOREA

JAPAN

TAIWAN

HONG

KONG

PHILLIPPINES

VIETNAM

THAILAND

INDIA

MALAYSIA

SINGAPORE INDONESIA

7.5%

4.9%

2.9%

3.0%

2.1%

3.0% 4.5%

-0.5%

3.6%

3.2%

-1.0%

7.0%

CB RICHARD ELLIS VIETNAM

5Where are we going? What have we learned? |September 2009

Linked Markets

Real estate capital values trend closely with domestic gold and stock prices

VN Index

Closed at

556.75

15 Sept 2009

130%

Source: HSC Securities

Vietnam Gold

15%

Source: Giavang

CB RICHARD ELLIS VIETNAM

6Where are we going? What have we learned? |September 2009

Office Rent Cycle

CB RICHARD ELLIS VIETNAM

7Where are we going? What have we learned? |September 2009

Complexity of deals

Investment Sales change shape

Foreigners to Locals

Locals to Foreigners

Sale of Shares of single asset companies

En-bloc Sales during construction

Sale of the Retail Podium of mixed-use developments

Sale of 1 tower (out of several)

MORE assets have changed hands but transactions are below the radar screen

More inside deals

Investors have become more particular with their requests and have tighter budgets

No A.A. in Vietnam

CB RICHARD ELLIS VIETNAM

8Where are we going? What have we learned? |September 2009

Increased competition

Pressure on owners, land lords and investors

Little differentiation of design, style and the theme

Commoditization of small office buildings

Stand out in the crowd

Small tenants still looking for space

Pay fees

CB RICHARD ELLIS VIETNAM

9Where are we going? What have we learned? |September 2009

Yields

Yield compression as rents fall

Tighter expected spreads

Longer paybacks

Developers will need creativity to create more value but compared to

Singapore, Hong Kong and China, they are still high

CB RICHARD ELLIS VIETNAM

10 Where are we going? What have we learned? |September 2009

Adding Value

Building Design

Refurbishment options

Example of retail developers in Causeway Bay (HK)

and Ginza (Tokyo)

%20--%3e%3cdefs%3e%3cstyle%3e%20.st0%20{%20fill:%20%23fff;%20}%20.st1%20{%20fill:%20%237800fa;%20}%20%3c/style%3e%3c/defs%3e%3cpath%20class='st1'%20d='M117.78,12.18H43.11c2.9,3.47,4.65,7.94,4.65,12.82,0,5.6-2.3,10.66-6.01,14.29h76.02l7.22-13.56-7.22-13.56Z'/%3e%3cg%3e%3cpath%20class='st0'%20d='M53.58,26.17h-.59v-1.46h.59v-4.96h2.83c1.78,0,2.67.94,2.67,2.82v5.76c0,1.87-.89,2.81-2.67,2.81h-2.83v-4.96ZM55.36,21.37v3.34h1.1v1.46h-1.1v3.34h1.01c.61,0,.91-.37.91-1.1v-5.93c0-.74-.3-1.1-.91-1.1h-1.01Z'/%3e%3cpath%20class='st0'%20d='M65.99,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM65.28,18.04c-.25.46-.51.77-.75.94-.21.15-.47.22-.79.22-.26,0-.57-.07-.92-.22l-.38-.15c-.14-.05-.26-.07-.37-.07-.3,0-.53.18-.71.54l-.91-.68c.25-.46.51-.77.75-.94.21-.14.48-.21.79-.21.26,0,.57.07.92.21l.38.15c.14.05.26.07.37.07.3,0,.53-.18.71-.54l.91.68ZM61.91,27.52h1.73l-.87-5.76-.87,5.76Z'/%3e%3cpath%20class='st0'%20d='M74.53,26.89v1.52c0,1.91-.89,2.86-2.67,2.86s-2.67-.95-2.67-2.86v-5.93c0-1.91.89-2.86,2.67-2.86s2.67.95,2.67,2.86v1.11h-1.69v-1.22c0-.75-.31-1.12-.93-1.12s-.93.37-.93,1.12v6.15c0,.74.31,1.11.93,1.11s.93-.37.93-1.11v-1.63h1.69Z'/%3e%3cpath%20class='st0'%20d='M81.4,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM75.9,19.2l1.52-1.91h1.71l1.51,1.91h-1.61l-.76-.95-.75.95h-1.61ZM77.32,27.52h1.73l-.87-5.76-.87,5.76ZM83.1,15.99l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M84.86,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM84.01,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M93.51,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM92.66,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M98.8,31.14h-1.79v-11.39h1.79v4.88h2.03v-4.88h1.83v11.39h-1.83v-4.88h-2.03v4.88Z'/%3e%3cpath%20class='st0'%20d='M105.36,24.55h2.46v1.62h-2.46v3.34h3.09v1.63h-4.88v-11.39h4.88v1.63h-3.09v3.18ZM108.17,17.29l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M112.2,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM111.35,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3c/g%3e%3ccircle%20class='st1'%20cx='25'%20cy='25'%20r='20'/%3e%3cpath%20class='st0'%20d='M32.78,19.27c2.92,0,4.43,2.55,5.28,5.33l.71,2.17c.14.38-.33.75-.71.75h-5.61c.19-.33.24-.71.09-1.08l-.75-2.45c-.43-1.32-.99-2.64-1.79-3.77.75-.57,1.65-.94,2.78-.94h0ZM25,18.38c3.25,0,4.9,2.78,5.89,5.89l.76,2.45c.14.42-.33.8-.8.8h-11.69c-.42,0-.94-.38-.8-.8l.75-2.45c.99-3.11,2.64-5.89,5.89-5.89h0ZM25,11.35c1.74,0,3.11,1.37,3.11,3.11s-1.37,3.11-3.11,3.11-3.11-1.41-3.11-3.11,1.41-3.11,3.11-3.11h0ZM17.27,19.27c1.08,0,1.98.38,2.73.94-.8,1.13-1.37,2.45-1.74,3.77l-.8,2.45c-.14.38-.05.75.09,1.08h-5.56c-.42,0-.9-.38-.75-.75l.71-2.17c.9-2.78,2.41-5.33,5.33-5.33h0ZM17.27,12.91c1.51,0,2.78,1.27,2.78,2.83s-1.27,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM32.78,12.91c1.56,0,2.78,1.27,2.78,2.83s-1.23,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM27.07,28.56v.09c0,.57-.24,1.08-.61,1.46h0v.05c-.38.33-.9.57-1.46.57s-1.08-.24-1.46-.61h0c-.38-.38-.61-.9-.61-1.46v-.09h1.41v.09c0,.19.05.38.19.47v.05c.09.09.28.19.47.19s.38-.09.47-.19v-.05c.14-.09.24-.28.24-.47t-.05-.09h1.41ZM30.99,28.56v.09c0,1.65-.66,3.16-1.74,4.24-1.08,1.08-2.59,1.79-4.24,1.79s-3.16-.71-4.24-1.79l-.05-.05c-1.04-1.08-1.7-2.55-1.7-4.2v-.09h1.41v.09c0,1.27.47,2.4,1.27,3.25h.05c.85.85,1.98,1.37,3.25,1.37s2.4-.52,3.25-1.37c.85-.8,1.37-1.98,1.37-3.25v-.09h1.37ZM34.99,28.56v.09c0,2.78-1.13,5.28-2.92,7.07-1.79,1.79-4.29,2.92-7.07,2.92s-5.23-1.13-7.07-2.92c-1.79-1.79-2.92-4.29-2.92-7.07v-.09h1.41v.09c0,2.4.94,4.53,2.5,6.08,1.56,1.56,3.72,2.5,6.08,2.5s4.52-.94,6.08-2.5c1.56-1.56,2.5-3.68,2.5-6.08v-.09h1.41Z'/%3e%3c/svg%3e)