6/13/2013

1

Các bằng chứng kiểm

toán đặc biệt

Chuyên đề 2

Trình bày: Nguyễn Trí Tri

BAÙO

CAÙO TAØI

CHÍNH

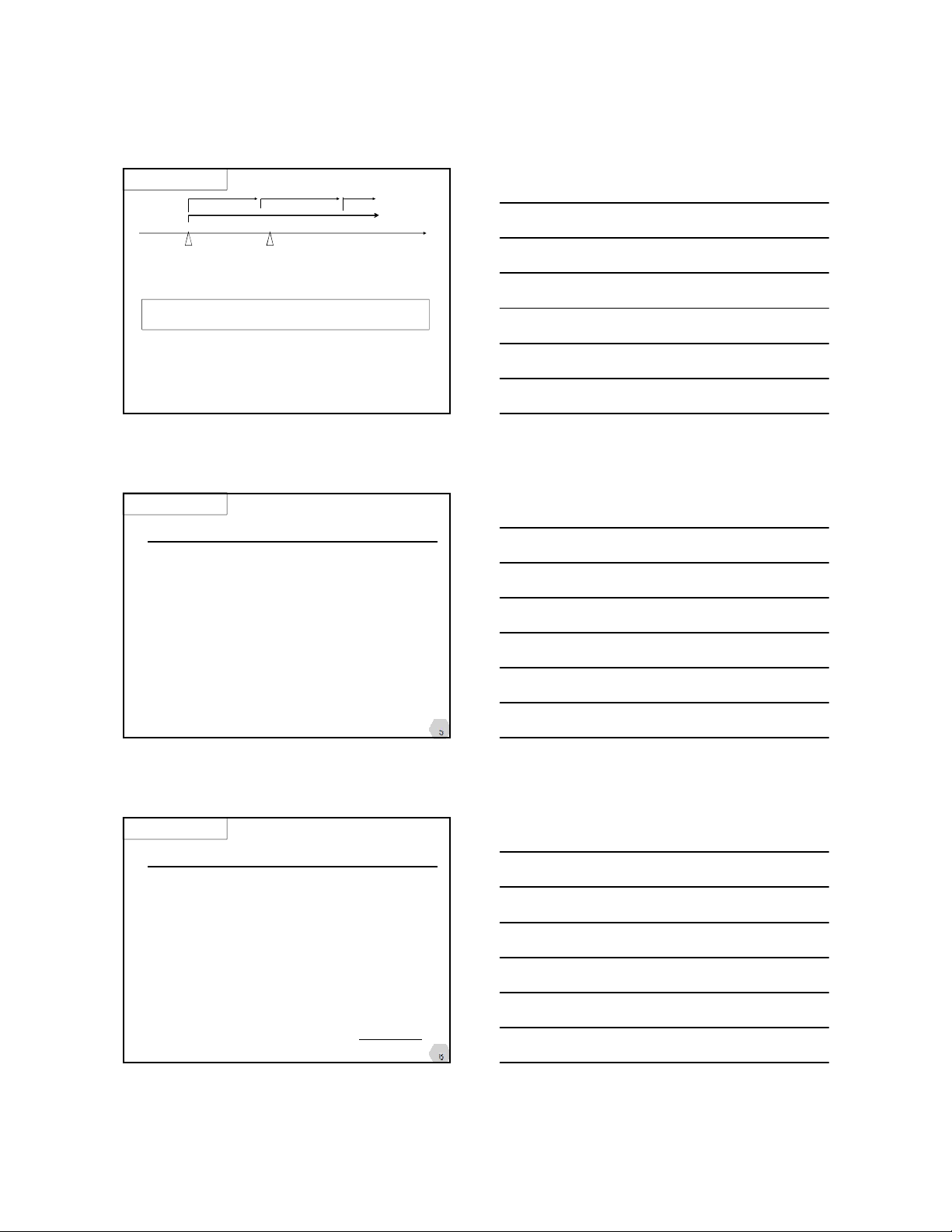

Caùc cô sôû daãn lieäu thoâng thöôøng

Soá dö ñaàu naêm

Öôùc tính keá toaùn

Söï kieän tieáp theo

Tính hoaït ñoäng lieân tuïc

Giaûi trình cuûa GÑ

Baèng

chöùng

kieåm toaùn

ñaëc bieät

Caùc beân lieân quan

Chöùng kieán kieåm keâ

Xaùc nhaän nôï phaûi thu

Nôï tieàm taøng

Söû duïng coâng vieäc beân khaùc

3

Söï kieän sau ngaøy khoùa soå

Nguoàn tham chieáu: VSA/ISA 560, VAS 23,

IAS 10

Khaùi nieäm

Phaân loaïi

Thuû tuïc kieåm toaùn

6/13/2013

2

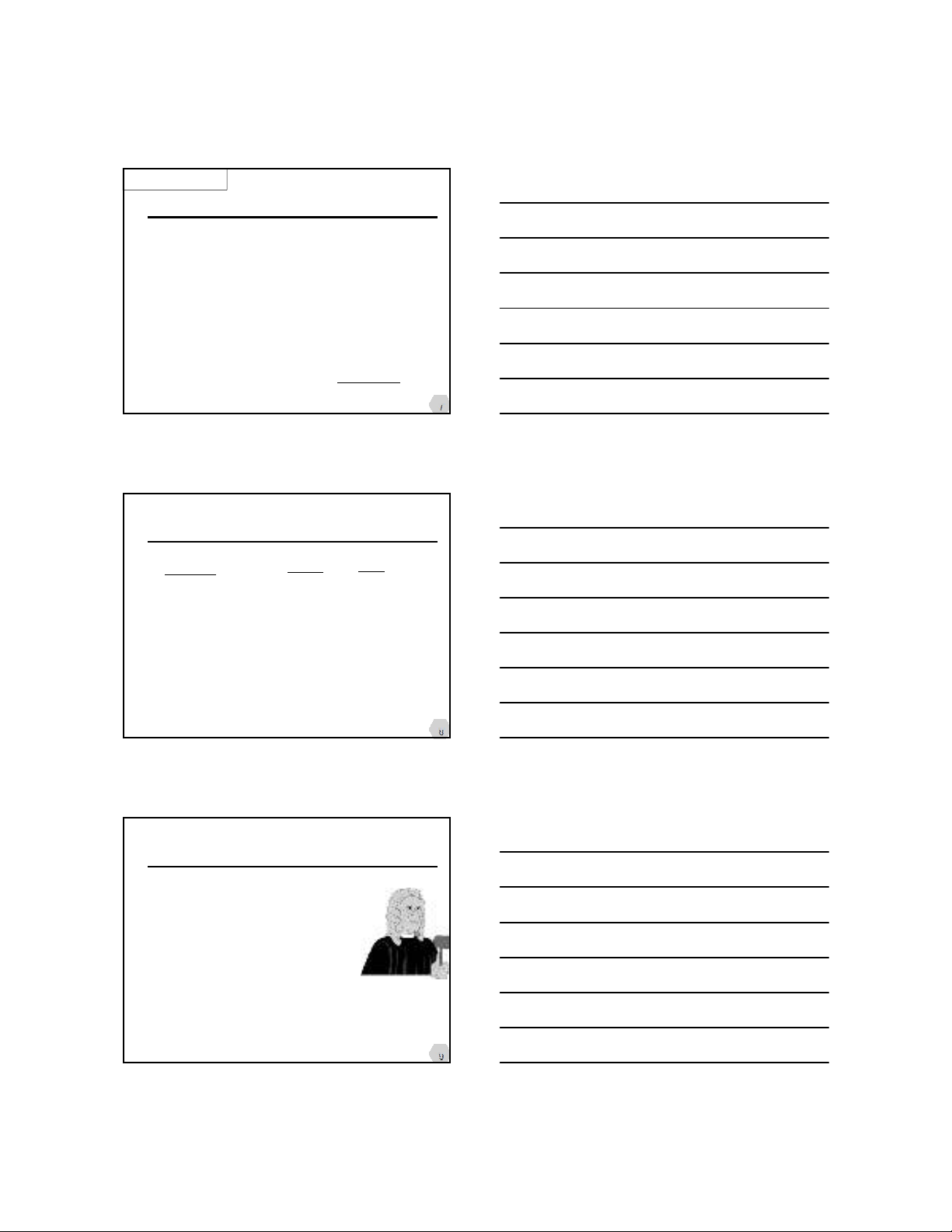

31.12.200X

Ngaøy keát thuùc

nieân ñoä

1.2.200X+1

Ngaøy phaùt

haønh BCTC

Söï kieän sau ngaøy khoùa soå keá toaùn laäp BCTC

(*)Söï kieän phaùt sinh sau ngaøy khoùa soå keá toaùn laäp BCTC

VAS 23

(*)

Ngày phát hành báo cáo tài chính: Là ngày, tháng, năm ghi

trên báo cáo tài chính mà Giám đốc (hoặc người được ủy

quyền) của đơn vị kế toán ký duyệt báo cáo tài chính để gửi

ra bên ngoài doanh nghiệp.

5

Events after the balance sheet date

Events after the balance sheet date are

those events, favourable and unfavourable,

that occur between the balance sheet date

and the date when the financial statements

are authorised for issue.

IAS 10

Be careful with the date of

authorisation for issue!!!

6

In some cases, an entity is required to submit its financial statements to its

shareholders for approval after the financial statements have been issued.

In such cases, the financial statements are authorised for issue on the

date of issue, not the date when shareholders approve the financial

statements.

Example

The management of an entity completes draft financial statements for the

year to 31 December 20X1 on 28 February 20X2. On 18 March 20X2, the

board of directors reviews the financial statements and authorises them

for issue. The entity announces its profit and selected other financial

information on 19 March 20X2. The financial statements are made

available to shareholders and others on 1 April 20X2. The shareholders

approve the financial statements at their annual meeting on 15 May 20X2

and the approved financial statements are then filed with a regulatory

body on 17 May 20X2.

The financial statements are authorised for issue on 18 March 20X2 (date

of board authorisation for issue).

Date of authorisation for issue

IAS 10

6/13/2013

3

7

In some cases, the management of an entity is required to issue its financial

statements to a supervisory board (made up solely of non-executives) for

approval. In such cases, the financial statements are authorised for issue when

the management authorises them for issue to the supervisory board.

Example

On 18 March 20X2, the management of an entity authorises financial

statements for issue to its supervisory board. The supervisory board is made up

solely of non-executives and may include representatives of employees and

other outside interests. The supervisory board approves the financial

statements on 26 March 20X2. The financial statements are made available to

shareholders and others on 1 April 20X2. The shareholders approve the

financial statements at their annual meeting on 15 May 20X2 and the financial

statements are then filed with a regulatory body on 17 May 20X2.

The financial statements are authorised for issue on 18 March 20X2 (date of

management authorisation for issue to the supervisory board).

Date of authorisation for issue (con’t)

IAS 10

8

Söï kieän phaùt sinh sau ngaøy khoùa soå laäp BCTC

Loaïi söï kieän

Nhöõng söï kieän cung

caáp theâm baèng chöùng

veà caùc söï vieäc ñaõ toàn

taïi vaøo ngaøy khoaù soå

keá toaùn laäp baùo caùo

taøi chính

Yeâu caàu

Ñieàu chænh

baùo caùo taøi

chính

Thí duï

Baùn taøi saûn hay

thu hoài coâng nôï

sau ngaøy keát

thuùc nieân ñoä

khaùc vôùi soá lieäu

soå saùch

Nhöõng söï kieän cung caáp

daáu hieäu veà caùc söï vieäc

ñaõ phaùt sinh tieáp sau

ngaøy khoaù soå keá toaùn

laäp Baùo caùo taøi chính

Khoâng caàn

ñieàu chænh,

nhöng coù theå

yeâu caàu khai

baùo

Phaùt haønh coå

phieáu sau ngaøy

khoùa soå

9

Thí dụ về các sự kiện phát sinh sau ngày

kết thúc kỳ kế toán năm cần điều chỉnh

Kết luận của Toà án sau ngày kết thúc kỳ kế

toán năm, xác nhận doanh nghiệp có những

nghĩa vụ hiện tại vào ngày kết thúc kỳ kế toán

năm, đòi hỏi doanh nghiệp điều chỉnh khoản

dự phòng đã được ghi nhận từ trước; ghi nhận

những khoản dự phòng mới hoặc ghi nhận

những khoản nợ phải thu, nợ phải trả mới.

Thông tin nhận được sau ngày kết thúc kỳ kế

toán năm cung cấp bằng chứng về một tài sản

bị tổn thất trong kỳ kế toán năm, hoặc giá trị

của khoản tổn thất được ghi nhận từ trước đối

với tài sản này cần phải điều chỉnh,

6/13/2013

4

10

Thí dụ về các sự kiện phát sinh sau ngày kết

thúc kỳ kế toán năm cần điều chỉnh (tt)

Việc xác nhận sau ngày kết thúc kỳ

kế toán năm về giá gốc của tài sản

đã mua hoặc số tiền thu được từ

việc bán tài sản trong kỳ kế toán

năm.

Việc phát hiện những gian lận và sai

sót chỉ ra rằng báo cáo tài chính

không được chính xác.

11

Thí dụ về các sự kiện phát sinh sau ngày kết

thúc kỳ kế toán năm không cần điều chỉnh

Việc hợp nhất kinh doanh hoặc việc thanh lý công ty

con của tập đoàn;

Việc công bố kế hoạch ngừng hoạt động, việc thanh

lý tài sản hoặc thanh toán các khoản nợ liên quan

đến ngừng hoạt động; hoặc việc tham gia vào một

hợp đồng ràng buộc để bán tài sản hoặc thanh toán

các khoản nợ;

Mua sắm hoặc thanh lý tài sản có giá trị lớn;

Nhà xưởng sản xuất bị phá hủy vì hỏa hoạn, bão lụt;

Thực hiện tái cơ cấu chủ yếu;

12

Thí dụ về các sự kiện phát sinh sau ngày kết

thúc kỳ kế toán năm không cần điều chỉnh (tt)

Các giao dịch chủ yếu và tiềm năng của cổ phiếu

thường;

Thay đổi bất thường, quan trọng về giá bán tài sản

hoặc tỷ giá hối đoái.

Thay đổi về thuế có ảnh hưởng quan trọng đến tài

sản, nợ thuế hiện hành hoặc thuế hoãn lại;

Tham gia những cam kết, thỏa thuận quan trọng

hoặc những khoản nợ tiềm tàng;

Xuất hiện những vụ kiện tụng lớn./.

6/13/2013

5

13

Minh họa -Trích Thuyết minh BCTC hợp nhất FPT 2008

14

Minh họa

Trích Thuyết minh BCTC hợp nhất FPT 2008

15

Minh họa

Preliminary Agreement with SANYO

On February 14, 2006, the Group and SANYO

Electric Co., Ltd announced a preliminary

agreement with intent to form a new global

company comprised of their respective CDMA

mobile phone businesses – separate from the

parent companies. The relevant assets from both

companies will be contributed or made available for

the new entity. Final agreements are expected to

be signed in the second quarter of 2006, with the

new business expected to commence operations in

the third quarter 2006, provided that the due

diligence has been completed and all necessary

regulatory approvals obtained.

Nguồn: Nokia’s financial statements for year ended

31.12.2005

![Bài giảng Kiểm toán căn bản: Chương 2 - TS. Nguyễn Thị Thanh Phương [Mới nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2024/20240420/khanhchi2520/135x160/49086127.jpg)

![Tập bài giảng Kiểm toán tài chính [chuẩn nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2021/20211119/cucngoainhan3/135x160/488611802.jpg)

![Bài giảng Kiểm toán: Bài 6 – PGS.TS. Phan Trung Kiên [Chuẩn Nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2021/20210107/trinhthamhodang1217/135x160/5141610009016.jpg)