1

RSM McGladrey, Inc. is a member firm of RSM International – an affiliation of separate and independent legal entities.

Integrated Audit

Presented by:

Hussain T. Hasan, CISM, CISSP

Managing Director

Technology Risk Management Services (TRMS)

Hussain.hasan@rsmi.com

IT and Finance - Are We Talking the Same Language?

2

Session Goals

• History and background of IT Audit

• Try to address the gap that exists between financial audit

and information technology audit

• What is involved in IT general controls and automated

application controls

• Discuss an approach that will aide in the identification and

testing of IT controls

• Roles and responsibilities for IT and financial auditors

2

3

History of IT Audits

• First use of a computerized accounting system - 1954 by GE

• Use of computer accounting systems became more prevalent

in mid-60s and early 70s

• AICPA and the “Big 8” formalize EDP auditing with the

release of the book “Auditing & EDP” - 1968

• Electronic Data Processing Auditors Association (EDPAA)

formed -late 1960s

• First edition of control objectives was published (now known

as CoBiT) - 1977

• EDPAA changes name to ISACA (Information Systems Audit

and Control Association) - 1994

4

Major Events Impacting IT Auditing

• Equity Funding Corporation of America fraud (1964 -1973)

• AT&T infrastructure failure -1998

• September 11th terrorist attacks - 2001

• Enron and Arthur Andersen - 2002

3

5

Why is IT Auditing a Challenge?

• Unlike the certification of financial statements there is no

“universally accepted principle or standard” for IT audit

• The concept of “compliance to best practice”

• Rapid change in IT is at times too rapid for best practices to

fully develop or be recognized as such

• IT audit has become a separate discipline over time

6

Today’s Business Process Environment

• 24/7 requirement becoming more common

• Focus on early error detection

• More highly automated – reducing reliance on manual

controls

• Integrated with complex and highly efficient IT systems

• Electronic workflow with paperless trails

• Increased business partner involvement through direct

access to process – the network extends beyond the

company

4

7

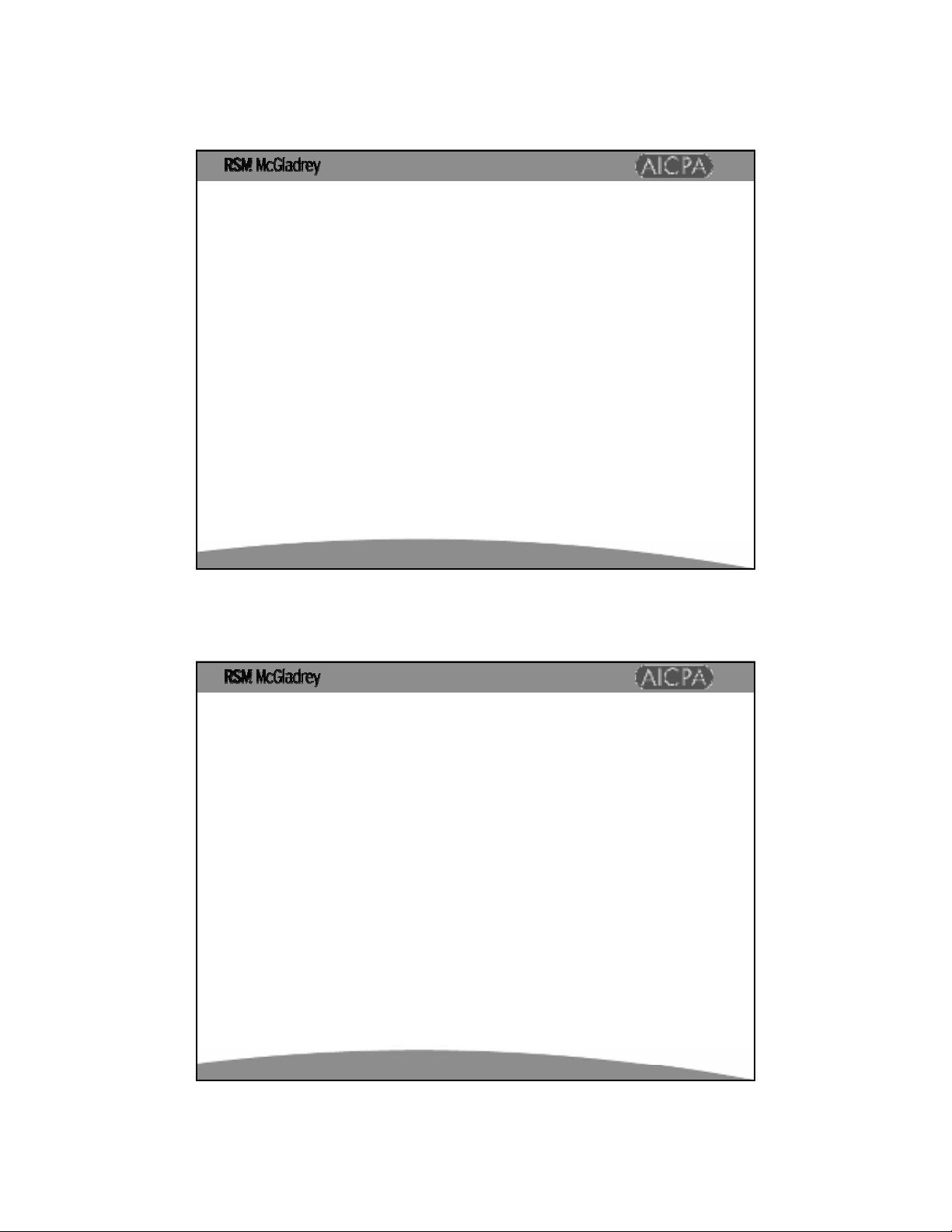

Application A

Financial Applications

Application B Application C

Process A

Business Processes/Classes of Transactions

Balance

Sheet

Significant Financial Transaction Accounts

Income

Statement SCFP Notes Other

Automated Application Controls

•Application Security

•Input Controls

•Process Controls

•Output Controls

•Interface Controls

IT General Controls

•Change/Development

•Security

•Computer Operations

•IT Governance

Source: Adapted from IT Governance Board, ISACA White Paper IT Control Objectives for Sarbanes-Oxley

Network

Operating System

Database

Infrastructure Services

Platform

Process B Class A Class B

IT Control Framework

8

IT General Controls (ITGC)

• IT general controls are pervasive controls within the IT

environment and the effectiveness of all automated

application controls across the organization depends on

them.

– Security (access to programs and data)

– Change / development

– Computer operations

– IT governance

• Primary responsibility of the IT Team

• Constant interaction with the Financial Audit Team

5

9

Automated Application Controls

• Application controls apply to the business processes they

support.

• These controls are embedded within the software

applications to prevent or detect unauthorized transactions.

• When combined with manual controls, application controls

ensure completeness, accuracy, authorization and validity

of processing transactions.

10

Automated Application Controls

• Automated application-based processes that control

access, input, output and reporting

• Typically set up in the software implementation phase, and

can be modified in the maintenance phase. Depending on

the software used, modification may be problematic.

• Degree of need for review partially dependent on software

used

• Also called IT controls or programmed control

![Giáo trình Tin học kế toán trình độ Cao đẳng, Trung cấp [mới nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260527/alfredodistefano10/135x160/12651780246460.jpg)

![Giáo trình Tài chính doanh nghiệp (Cao đẳng, Trung cấp): [Hướng dẫn/Tài liệu/Bài tập]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260527/alfredodistefano10/135x160/73771780246461.jpg)

![Giáo trình Quản trị học trình độ Cao đẳng, Trung cấp [Chuẩn nhất]](https://cdn.tailieu.vn/images/document/thumbnail/2026/20260527/alfredodistefano10/135x160/51311780246462.jpg)

%20--%3e%3cdefs%3e%3cstyle%3e%20.st0%20{%20fill:%20%23fff;%20}%20.st1%20{%20fill:%20%237800fa;%20}%20%3c/style%3e%3c/defs%3e%3cpath%20class='st1'%20d='M117.78,12.18H43.11c2.9,3.47,4.65,7.94,4.65,12.82,0,5.6-2.3,10.66-6.01,14.29h76.02l7.22-13.56-7.22-13.56Z'/%3e%3cg%3e%3cpath%20class='st0'%20d='M53.58,26.17h-.59v-1.46h.59v-4.96h2.83c1.78,0,2.67.94,2.67,2.82v5.76c0,1.87-.89,2.81-2.67,2.81h-2.83v-4.96ZM55.36,21.37v3.34h1.1v1.46h-1.1v3.34h1.01c.61,0,.91-.37.91-1.1v-5.93c0-.74-.3-1.1-.91-1.1h-1.01Z'/%3e%3cpath%20class='st0'%20d='M65.99,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM65.28,18.04c-.25.46-.51.77-.75.94-.21.15-.47.22-.79.22-.26,0-.57-.07-.92-.22l-.38-.15c-.14-.05-.26-.07-.37-.07-.3,0-.53.18-.71.54l-.91-.68c.25-.46.51-.77.75-.94.21-.14.48-.21.79-.21.26,0,.57.07.92.21l.38.15c.14.05.26.07.37.07.3,0,.53-.18.71-.54l.91.68ZM61.91,27.52h1.73l-.87-5.76-.87,5.76Z'/%3e%3cpath%20class='st0'%20d='M74.53,26.89v1.52c0,1.91-.89,2.86-2.67,2.86s-2.67-.95-2.67-2.86v-5.93c0-1.91.89-2.86,2.67-2.86s2.67.95,2.67,2.86v1.11h-1.69v-1.22c0-.75-.31-1.12-.93-1.12s-.93.37-.93,1.12v6.15c0,.74.31,1.11.93,1.11s.93-.37.93-1.11v-1.63h1.69Z'/%3e%3cpath%20class='st0'%20d='M81.4,31.14h-1.8l-.31-2.07h-2.19l-.31,2.07h-1.64l1.82-11.39h2.62l1.82,11.39ZM75.9,19.2l1.52-1.91h1.71l1.51,1.91h-1.61l-.76-.95-.75.95h-1.61ZM77.32,27.52h1.73l-.87-5.76-.87,5.76ZM83.1,15.99l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M84.86,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM84.01,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M93.51,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM92.66,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3cpath%20class='st0'%20d='M98.8,31.14h-1.79v-11.39h1.79v4.88h2.03v-4.88h1.83v11.39h-1.83v-4.88h-2.03v4.88Z'/%3e%3cpath%20class='st0'%20d='M105.36,24.55h2.46v1.62h-2.46v3.34h3.09v1.63h-4.88v-11.39h4.88v1.63h-3.09v3.18ZM108.17,17.29l-1.76,1.91h-1.26l1.17-1.91h1.86Z'/%3e%3cpath%20class='st0'%20d='M112.2,19.75c1.78,0,2.67.94,2.67,2.82v1.48c0,1.87-.89,2.81-2.67,2.81h-.85v4.28h-1.79v-11.39h2.64ZM111.35,21.37v3.86h.85c.58,0,.87-.36.87-1.08v-1.71c0-.71-.29-1.07-.87-1.07h-.85Z'/%3e%3c/g%3e%3ccircle%20class='st1'%20cx='25'%20cy='25'%20r='20'/%3e%3cpath%20class='st0'%20d='M32.78,19.27c2.92,0,4.43,2.55,5.28,5.33l.71,2.17c.14.38-.33.75-.71.75h-5.61c.19-.33.24-.71.09-1.08l-.75-2.45c-.43-1.32-.99-2.64-1.79-3.77.75-.57,1.65-.94,2.78-.94h0ZM25,18.38c3.25,0,4.9,2.78,5.89,5.89l.76,2.45c.14.42-.33.8-.8.8h-11.69c-.42,0-.94-.38-.8-.8l.75-2.45c.99-3.11,2.64-5.89,5.89-5.89h0ZM25,11.35c1.74,0,3.11,1.37,3.11,3.11s-1.37,3.11-3.11,3.11-3.11-1.41-3.11-3.11,1.41-3.11,3.11-3.11h0ZM17.27,19.27c1.08,0,1.98.38,2.73.94-.8,1.13-1.37,2.45-1.74,3.77l-.8,2.45c-.14.38-.05.75.09,1.08h-5.56c-.42,0-.9-.38-.75-.75l.71-2.17c.9-2.78,2.41-5.33,5.33-5.33h0ZM17.27,12.91c1.51,0,2.78,1.27,2.78,2.83s-1.27,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM32.78,12.91c1.56,0,2.78,1.27,2.78,2.83s-1.23,2.83-2.78,2.83-2.83-1.27-2.83-2.83,1.27-2.83,2.83-2.83h0ZM27.07,28.56v.09c0,.57-.24,1.08-.61,1.46h0v.05c-.38.33-.9.57-1.46.57s-1.08-.24-1.46-.61h0c-.38-.38-.61-.9-.61-1.46v-.09h1.41v.09c0,.19.05.38.19.47v.05c.09.09.28.19.47.19s.38-.09.47-.19v-.05c.14-.09.24-.28.24-.47t-.05-.09h1.41ZM30.99,28.56v.09c0,1.65-.66,3.16-1.74,4.24-1.08,1.08-2.59,1.79-4.24,1.79s-3.16-.71-4.24-1.79l-.05-.05c-1.04-1.08-1.7-2.55-1.7-4.2v-.09h1.41v.09c0,1.27.47,2.4,1.27,3.25h.05c.85.85,1.98,1.37,3.25,1.37s2.4-.52,3.25-1.37c.85-.8,1.37-1.98,1.37-3.25v-.09h1.37ZM34.99,28.56v.09c0,2.78-1.13,5.28-2.92,7.07-1.79,1.79-4.29,2.92-7.07,2.92s-5.23-1.13-7.07-2.92c-1.79-1.79-2.92-4.29-2.92-7.07v-.09h1.41v.09c0,2.4.94,4.53,2.5,6.08,1.56,1.56,3.72,2.5,6.08,2.5s4.52-.94,6.08-2.5c1.56-1.56,2.5-3.68,2.5-6.08v-.09h1.41Z'/%3e%3c/svg%3e)